Advertorial or Sponsorship User published Content does not represent the views of the Company or any individual associated with the Company, and we do not control this Content. In no event shall you represent or suggest, directly or indirectly, the Company's endorsement of user published Content.

The company does not vouch for the accuracy or credibility of any user published Content on our Website and does not take any responsibility or assume any liability for any actions you may take as a result of reading user published Content on our Website.

Through your use of the Website and Services, you may be exposed to Content that you may find offensive, objectionable, harmful, inaccurate, or deceptive.

By using our Website, you assume all associated risks.This Website contains hyperlinks to other websites controlled by third parties. These links are provided solely as a convenience to you and do not imply endorsement by the Company of, or any affiliation with, or endorsement by, the owner of the linked website.

Company is not responsible for the contents or use of any linked website, or any consequence of making the link.

Fora Financial Reviews and Ratings (2026)

Fora Financial Official Logo

Small business owners with less-than-perfect credit often face a frustrating reality. Traditional banks require months of paperwork and stellar credit scores. This leaves many entrepreneurs with few options when they need capital quickly.

With changes to small-business regulations and tax requirements in 2025, understanding your financing options is more critical than ever. This Fora Financial reviews guide examines whether this New York-based alternative lender delivers on its promise. We analyze whether they provide fast funding with flexible requirements. Or if the higher costs and recent data breach concerns should give borrowers pause.

We analyze Better Business Bureau complaint history, Trustpilot ratings, factor rate structures, data breach disclosure, and real customer experiences. This helps you determine if Fora Financial is worth considering for your working capital needs

TD; LR: Quick verdict

Our rating: 3.5/5

Reputation and trust:

- BBB rating: A+ (accredited since Jan. 20, 2011)

- BBB complaints: Six to seven in the last three years

- BBB customer reviews: 2.73/5 (11 reviews)

- Trustpilot: 4.6/5 (987 reviews)

Funding essentials:

- Funding range: $5,000 to $1,500,000

- Factor rates: 1.13-1.40 (equivalent to 13-40 cents per dollar borrowed)

- Repayment terms: Four to 15 months (some sources say up to 18-24 months)

The bottom line:

- Best for: Established businesses with $20,000-plus monthly revenue needing fast capital despite higher costs

- Data breach note: September 2022 cybersecurity incident affected approximately 3,200 individuals — 12 months free credit monitoring offered

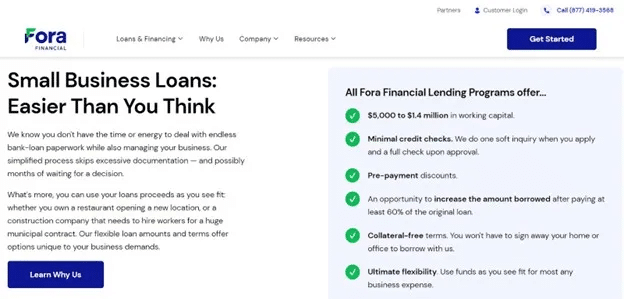

What is Fora Financial?

Fora Financial homepage

Fora Financial is a New York-based alternative lender. They have been providing working capital to small businesses since 2008. Originally founded as Paramount Merchant Funding LLC, the company rebranded to Fora Financial in 2013.

The company was founded by college roommates Jared Feldman and Daniel Smith. They met while studying business management at Indiana University. Both had prior experience working at Merchant Cash & Capital (now BizFi) before launching their own venture on June 16, 2008.

Company background

- Entity type: Limited liability company

- Headquarters: 1385 Broadway, 15th Floor, New York, NY 10018

- BBB rating: A+ (accredited Jan. 20, 2011; file opened Nov. 5, 2010)

- Years in business: 17 years (founded 2008)

- Employees: Approximately 180

- Total funding distributed: More than $4 billion to over 55,000 small businesses

- Ownership: Backed by Palladium Equity Partners LLC (majority stake acquired October 2015)

- Acquisitions: United States Business Funding (2018)

- Recognition: Inc. 5000 list for six consecutive years; Best Financial Services Company of the Year at American Business Awards

- Financial capacity: $130 million revolving credit facility plus $10 million investment-grade rated corporate note

Leadership team

Jared Feldman serves as chief executive officer and co-founder. Daniel Smith remains involved as co-founder and board member after serving as president from 2008 to 2020.

The executive team also includes a CFO named John, a COO named Jesse, CMO Elissa Feldman and General Counsel John Viskocil. Fora Financial has also opened an additional office in downtown Miami, Florida.

Evaluate these top-rated lenders to find a better match for your credit tier:

- Direct Lending Excellence: Matches you with the best loans.

- Loans ranging from $2,500 to $100,000

- Flexible terms: 3 to 120 months, 24 hours post-approval

- Same day approval

-

Your Best Lending Partner: We match you with top lenders for the best deals.

-

Fast, Easy Process: Quick approvals with expert support.

-

Tailored Solutions: Flexible terms that fit your needs.

- Your Best Lending Partner: Rated #1 for customer satisfaction and personalized service.

- Fast, Easy Approvals: Get funded in as little as 24 hours with zero hidden fees.

- Tailored Loan Solutions: Flexible terms designed around your financial goals.

How Fora Financial works

Fora Financial operates as a direct lender. This means the company funds loans directly rather than acting as a broker. The company started as a loan broker but has since transitioned to direct funding. They use a proprietary underwriting technology platform.

This focus targets businesses that may not qualify for traditional bank financing due to credit history or other factors. The company offers two primary funding products: Small Business Loans and Revenue Advances. Both products provide funding amounts ranging from $5,000 to $1,500,000. However, the repayment structures differ significantly.

Small Business Loans

Small Business Loans function as term loans with fixed repayment schedules. Funding amounts range from $5,000 to $1,500,000, with terms of 4 to 15 months.

Some sources indicate terms may extend to 18-24 months. Payments are collected daily or weekly via automatic ACH debits from your business bank account.

These loans work best for one-time expenses. Examples include equipment purchases or business expansion projects that require a lump sum and allow you to commit to a fixed repayment schedule.

Revenue Advances

Revenue Advances operate similarly to merchant cash advances. Payments are based on a fixed percentage of your daily or weekly gross receipts.

This structure provides more flexibility for businesses with variable income. Payments automatically scale with revenue fluctuations. The funding range remains $5,000 to $1,500,000. This option is particularly suitable for seasonal businesses or companies with inconsistent cash flow patterns.

Qualification requirements

To qualify for Fora Financial funding, businesses must meet several baseline requirements:

- Minimum credit score: 570 (some sources indicate 500 may be accepted)

- Time in business: At least six months

- Monthly revenue: Minimum $20,000 ($240,000 annually)

- No open bankruptcies

- Business bank account required

- Three months of bank statements

Application process

The Fora Financial application process emphasizes speed:

- Apply: Complete the one-page online application in minutes.

- Upload documents: Submit three months of business bank statements.

- Consultation: Speak with a Capital Specialist or Relationship Manager to discuss your needs.

- Approval: Receive an approval decision in as fast as four hours.

- Review offer: Examine and accept the funding offer.

- Receive funds: Funds are deposited within 24-72 hours of acceptance.

Fora Financial fees and pricing

Fora Financial uses factor rates rather than traditional annual percentage rates. This can make cost comparison challenging. Factor rates typically range from 1.13 to 1.40. This translates to 13-40 cents per dollar borrowed. According to LendingTree, factor rates can reach 1.40 for some borrowers.

For borrowers who pay back early, factor rates can be reduced to as low as 1.10. However, this depends on the specific terms of your agreement.

Understanding factor rates

A factor rate determines your total repayment amount. It works by multiplying the loan principal by the factor. For example, a $10,000 loan with a 1.30 factor rate results in a total repayment of $13,000. This represents a 30 percent cost on the principal amount.

Unlike annual percentage rates, factor rates do not account for the repayment term. This creates confusion when comparing costs. When converted to APR, a 1.30 factor rate over 12 months approximates 63-65 percent APR. The same factor rate over six months can exceed 125 percent APR.

This structure makes direct comparison with traditional bank loans difficult. The true cost depends heavily on how quickly you repay the advance.

Additional fees

Fora Financial charges a 3 percent origination fee based on the loan amount. The company also charges a wire transfer fee, though the exact amount is not publicly disclosed. The company does not charge prepayment penalties. Early payback discounts are available for qualifying borrowers. Payments are automatically collected via ACH debit from your business checking account. Collections occur either daily or weekly, depending on your agreement terms.

Cost comparison

Fora Financial’s rates are significantly higher than those of traditional banks. The average bank term loan carries an APR of approximately 7.98 percent for qualified borrowers.

However, Fora Financial’s rates remain competitive within the alternative lending space. The trade-off centers on speed and accessibility versus cost. Businesses that can qualify for traditional bank loans or Small Business Administration financing will find substantially lower rates through those channels.

However, companies with credit challenges or urgent timing needs may find Fora Financial’s higher costs acceptable. The trade-off is faster access to capital.

Many customer reviews cite high costs as a primary concern. Others appreciate the early payback discount option. The daily or weekly payment structure can strain cash flow for some businesses. This is particularly true for those with inconsistent revenue.

Fora Financial reviews and complaints

Fora Financial maintains generally positive reviews across multiple platforms. However, the feedback reveals both strengths and concerns that prospective borrowers should consider.

Better Business Bureau profile

Fora Financial A+ BBB Rating and Company Details

The company holds an A+ BBB rating with accreditation dating to January19, 2011, according to its Better Business Bureau profile. Over the past three years, Fora Financial has received eight total complaints. This is relatively low for a lender that has funded more than $4 billion.

Fora Financial BBB Complaint History

The BBB profile shows 12 customer reviews averaging 2.58 out of five stars. The mixed BBB reviews include both highly positive experiences and critical feedback. Some reviewers use terms like “loan sharks” to describe their experience with the cost structure.

Trustpilot reviews

Fora Financial Trustpilot profile

Fora Financial earns a 4.6 out of five rating on Trustpilot, labeled “Excellent,” based on 987 reviews as of February 2026. This represents a stark contrast to the BBB customer review average. It suggests generally positive borrower experiences.

A notable trend in Trustpilot reviews is the frequency with which customers mention specific Capital Specialists by name. These include Mitchell Sapoff, George James, Craig Burton, Patrick Ellman, Johnny Rodriguez, and Matt.

This pattern suggests a high level of individual attention and relationship building. The majority of reviews praise the speed of the funding process and the professionalism of the customer service team.

Reddit reviews

Reddit discussions on communities like r/loansforsmallbusiness generally confirm Fora Financial as a legitimate company. They may approve applications when traditional banks decline.

However, users consistently warn that they expect to pay high rates for this accessibility. Some describe the costs as the trade-off for speed and flexible requirements.

Common positive themes

Customers consistently praise several aspects of working with Fora Financial:

- Fast funding process, with many receiving funds within 24-72 hours

- Easy, streamlined online application taking just minutes to complete

- Professional and helpful Capital Specialists who build relationships with borrowers

- Flexible qualification requirements, particularly the 570 minimum credit score

- No collateral required for most funding products

- Approval when traditional banks have declined applications

- High repeat customer rate indicating satisfaction

- Early payback discounts for those able to repay quickly

Common complaints

Despite the positive feedback, several concerns appear repeatedly in customer reviews:

- High factor rates translate to expensive financing compared to traditional options

- Daily or weekly automatic payments can strain business cash flow

- Some borrowers report approved loan amounts being reduced after initial approval

- Factor rate structure makes cost comparison with traditional loans difficult

- Reports of aggressive follow-up calls and spam after initial inquiry

- Inconsistent customer service experiences from some borrowers

- Payments not reported to credit bureaus, missing an opportunity to build business credit

- September 2022 data breach affecting approximately 3,200 individuals

- BBB complaints about unsolicited marketing mailings

Company response pattern

Fora Financial demonstrates active engagement on the Better Business Bureau platform. They respond professionally to complaints and work to resolve issues. Some complaints have been resolved to customer satisfaction, showing the company’s willingness to address concerns.

Fora Financial data breach and security concerns

In September 2022, Fora Financial experienced a cybersecurity incident. Prospective borrowers should understand this before providing sensitive personal and financial information.

Breach timeline and details

The incident occurred on or about Sept. 9, 2022. It was discovered by the company that same month. Fora Financial identified and resolved the security vulnerability by Feb. 19, 2023.

Notification to affected individuals was delayed until 2023. This was due to the time required to analyze the compromised data. Approximately 3,200 individuals were potentially affected by the breach.

Data potentially compromised

The breach potentially exposed several categories of sensitive information:

- Names

- Dates of birth

- Government identification numbers (driver’s license or passport numbers)

- Social Security numbers

- Business financial data

Company response

Following the discovery of the breach, Fora Financial launched an immediate investigation. They engaged a forensic team to identify the vulnerability. The company resolved the security issue by February 2023.

Fora Financial offered 12 months of free credit monitoring and identity theft protection services to all affected individuals. Notifications were sent to affected individuals by mail once the data analysis was complete.

Legal status

As of January 2024, a class action investigation was ongoing. The law firm Abington Cole + Ellery was investigating potential claims related to the breach. No settlement has been announced as of the current research.

What this means for borrowers

Prospective borrowers should consider the data security implications as part of their due diligence. The breach does not necessarily indicate ongoing security issues, especially given the remediation efforts.

However, it remains a factor in the decision-making process. If you have applied to Fora Financial at any point, monitoring your credit reports and watching for signs of identity theft would be prudent steps.

Fora Financial outcomes and success rate

Fora Financial reports having funded more than $4 billion to small businesses since its founding in 2008. The company has served over 55,000 companies during that time. Fora Financial positions itself as an established player in the alternative lending market with 17 years of operating history.

Funding capacity and backing

The company operates with a $130 million revolving credit facility and a $10 million investment-grade rated corporate note. This institutional backing from Palladium Equity Partners provides financial stability.

Palladium Equity Partners acquired a majority stake in October 2015. Between 2015 and 2018, Fora Financial reported 105 percent growth.

Approval likelihood factors

The company’s relatively low credit score requirement of 570 minimum makes approval more accessible. Just six months of business history is required. This is more flexible than traditional bank financing.

The underwriting model focuses on revenue-based assessment rather than purely credit-focused evaluation. However, the $20,000 monthly revenue requirement creates a higher barrier than some competing alternative lenders.

Typical qualification ranges from 75 to 125 percent of monthly gross sales. This means businesses need consistent revenue to qualify for meaningful funding amounts.

Customer retention indicators

Multiple Trustpilot reviews mention repeat customers returning to Fora Financial for additional funding. This suggests satisfaction levels sufficient to prompt return business.

Several reviews specifically praise the company for funding businesses when traditional banks had declined their applications. The fast approval timeline of as little as four hours receives consistent positive mention.

Funding within 24-72 hours is consistently praised across review platforms.

Risk considerations

The daily or weekly payment structure can create cash flow challenges. This is particularly true for businesses with inconsistent revenue. High interest rates ranging from 1.15 to 1.40 make the financing expensive.

Short repayment terms of four to 15 months require rapid repayment. Because Fora Financial does not report payments to credit bureaus, on-time payment does not help build business credit.

The September 2022 data breach affecting approximately 3,200 individuals also raises security concerns. Borrowers should weigh these factors when deciding whether to provide sensitive information.

These factors do not necessarily preclude using Fora Financial. However, they require careful consideration of whether the speed and accessibility justify the higher costs and potential risks.

Fora Financial pros and cons

Advantages

- A+ BBB rating with more than 14 years of accreditation since 2011

- Strong Trustpilot rating of 4.6 out of five from 976 reviews

- Fast approval in as little as four hours and funding within 24-72 hours

- Low minimum credit score requirement of 570

- No collateral required for most funding products

- High funding amounts available up to $1.5 million

- Early payback discounts with factor rates as low as 1.10 for qualifying borrowers

- Flexible qualification requirements compared to traditional banks

- 17 years in business, demonstrating longevity and track record

- Professional customer service noted by the majority of reviews

- Inc. 5000 company for six consecutive years

- Institutional backing from Palladium Equity Partner’s providing financial stability

Disadvantages

- High factor rates of 1.13-1.40, equivalent to 30 percent-plus APR

- Daily or weekly automatic payments can strain cash flow

- Factor rate pricing structure makes cost comparison difficult

- Charges 3 percent origination fee based on loan amount

- Does not report to credit bureaus, missing opportunity to build business credit

- Short repayment terms of four to 15 months maximum

- High revenue requirement of $20,000 per month minimum

- September 2022 data breach affected approximately 3,200 individuals

- Class action investigation ongoing as of January 2024

- Some BBB reviews describe the company using terms like “loan sharks”

- Reports of loan amounts being reduced after initial approval

- Complaints about unsolicited marketing mail

Who should use Fora Financial?

Good fit

Fora Financial may work well for:

- Established businesses with at least six months of operating history

- Companies generating $20,000-plus in monthly revenue

- Business owners with credit scores of 570 or higher who cannot qualify for traditional bank loans

- Those needing capital quickly, within 24-72 hours

- Businesses that can sustain daily or weekly automatic payments without cash flow problems

- Companies with short-term working capital needs

- Businesses that have been declined by traditional lenders

Poor fit

Fora Financial may not be suitable for:

- Startups with less than six months of business history

- Businesses generating less than $20,000 in monthly revenue

- Companies seeking low-cost, long-term financing

- Businesses that cannot handle daily or weekly automatic payment withdrawals

- Borrowers are uncomfortable with factor rate pricing structures

- Companies needing to build business credit through reported payments

- Those with security or privacy concerns given the 2022 data breach history

Questions to ask before applying

Before submitting an application to Fora Financial, consider these questions:

- Can my business sustain daily or weekly automatic payment withdrawals?

- Do I meet the $20,000 monthly revenue requirement consistently?

- Have I calculated the true APR equivalent of the factor rate being offered?

- Am I comfortable with the company’s data breach history?

- Have I compared offers from multiple alternative lenders?

- Would I qualify for lower-cost options like SBA loans or bank lines of credit?

Fora Financial alternatives

Several alternatives exist for businesses seeking working capital. Each has different qualification requirements and cost structures.

Traditional financing options

Bank term loans offer the lowest rates for qualified borrowers. They average approximately 7-8 percent APR. Small Business Administration 7(a) loans provide government-backed rates up to $5 million.

However, the application process takes longer and requires more documentation. Credit unions often provide more personalized service with competitive rates for members.

Community development financial institutions specialize in serving underbanked communities. They may offer more flexible terms than traditional banks.

Do-it-yourself alternatives

SBA microloans offer smaller amounts with lower rates but slower processing. Business credit cards with zero percent introductory APR periods can provide short-term financing.

Invoice factoring converts outstanding receivables into immediate cash. Equipment financing provides funds specifically for equipment purchases.

Payment processor financing through companies like PayPal, Square or Stripe Capital offers quick access. Small business owners expecting tax refunds may also want to understand IRS processing timelines when planning their cash flow needs.

How Fora Financial compares

Fora Financial is more established than many competitors, with 17 years of operating history. The $20,000 monthly revenue requirement is higher than some alternative lenders, which can exclude smaller businesses.

Factor rates appear comparable to industry standards for alternative lenders. The September 2022 data breach represents a negative differentiator compared to competitors without such incidents.

Like most alternative lenders, Fora Financial does not report payments to credit bureaus. This misses opportunities to help borrowers build business credit.

Businesses should compare offers from at least three lenders before committing. This ensures they are getting competitive terms for their specific situation.

How to protect yourself from merchant cash advance scams

The alternative lending space attracts both legitimate companies and predatory actors. Understanding warning signs helps protect your business from scams.

Red flags to watch for

- Factor rates not disclosed until after you have provided extensive personal and financial information

- Pressure to sign agreements immediately without time to review terms

- F rating on Better Business Bureau or multiple unanswered complaints

- Closing costs or fees not clearly disclosed upfront

- No physical business address or legitimate contact information

- Very aggressive sales tactics or repeated unwanted phone calls

- Promises that seem too good to be true, such as guaranteed approval regardless of credit

Before signing any agreement

Take these steps to protect yourself:

- Get all fees and costs in writing before providing bank statements or other sensitive documents

- Calculate the true APR equivalent, not just the factor rate

- Understand exactly when payments start and the amount of each payment

- Ask what happens if your revenue drops and you cannot make scheduled payments

- Research the company on Better Business Bureau, Trustpilot and through general web searches

- Search for any data breaches or security incidents in the company’s history

- Read the entire contract before signing, not just the summary page

- Compare offers from at least three lenders to ensure competitive terms

If you encounter problems

- Document all communications with the lender, including emails, letters and notes from phone calls

- File a complaint with the Better Business Bureau immediately

- Contact your bank if unauthorized withdrawals occur

- Consider consulting a business attorney if you believe predatory practices are involved

- Report suspected predatory lending to your state attorney general

With Fora Financial specifically

Be aware of data breach history before providing sensitive information. Verify all terms in writing. Understand factor rate and calculate true APR.

Confirm early payback discount terms. Contact customer service at (212) 947-0100 or (855) 326-8525 for issues.

Fora Financial contact information

Phone: (212) 947-0100

Toll-free: (855) 326-8525 or (877) 514-8062

Fax: (888) 853-1437

Email: info@forafinancial.com

Address: 1385 Broadway, 15th Floor, New York, NY 10018

Website: forafinancial.com

Additional office: Downtown Miami, Florida

Leadership:

- Jared Feldman, CEO and co-founder

- Daniel Smith, co-founder and board member

Frequently asked questions

Is Fora Financial legit?

Yes, Fora Financial is a legitimate alternative lender founded in 2008 and headquartered in New York City. They are BBB accredited with an A+ rating since 2011 and have funded more than $4 billion to over 55,000 small businesses. Fora Financial is backed by Palladium Equity Partners and has been named to the Inc. 5000 list for six consecutive years. However, prospective borrowers should be aware of the September 2022 data breach that affected approximately 3,200 individuals and the ongoing class action investigation.

What are Fora Financial’s interest rates?

Fora Financial uses factor rates rather than traditional interest rates. Their factor rates typically range from 1.13 to 1.40, which translates to 13-40 cents per dollar borrowed. For example, a $10,000 loan at a 1.30 factor rate would require $13,000 in total repayment. Early payback provisions can reduce the factor rate to as low as 1.10. When converted to APR, these factor rates can equate to 30 percent to over 100 percent depending on the repayment term length.

What are the requirements to qualify for Fora Financial?

To qualify for Fora Financial, you need a minimum credit score of 570, at least six months in business and minimum monthly revenue of $20,000 ($240,000 annually). You cannot have any open bankruptcies. You will need to provide three months of business bank statements. Depending on the funding amount, Fora Financial may also require profit and loss statements, balance sheets and recent business tax returns.

How fast can you get funded with Fora Financial?

Fora Financial offers one of the faster funding timelines among alternative lenders. Their online application takes just minutes to complete, and approval decisions can come in as fast as four hours. Once you accept an offer, funds are typically deposited within 24-72 hours. Many customer reviews confirm receiving funding within 24-48 hours of acceptance.

Does Fora Financial have hidden fees?

Fora Financial charges a 3 percent origination fee based on the loan amount. They use a factor rate pricing model rather than traditional interest, which some borrowers find confusing. There are no prepayment penalties, and early payback can reduce your factor rate. However, the factor rate structure can make it difficult to compare total costs with traditional lenders. Always request a complete breakdown of all fees and the total repayment amount in writing before signing.

Fora Financial reviews final verdict

Fora Financial reviews reveal a well-established alternative lender with a 17-year track record. They have funded more than $4 billion to 55,000-plus businesses.

The A+ BBB rating has been maintained since 2011 and a 4.6 out of five Trustpilot score from 987 reviews demonstrates generally positive customer experiences. This is particularly true around speed and accessibility.

However, prospective borrowers must weigh several concerns. Factor rates of 1.13-1.40 translate to expensive financing with APR equivalents exceeding 30 percent. Daily or weekly automatic payments can strain cash flow for businesses with inconsistent revenue. The September 2022 data breach affecting 3,200 individuals raises security questions. The high $20,000 monthly revenue requirement also excludes many small businesses.

Recommendation

Fora Financial may be worth considering if you operate an established business with strong revenue exceeding $20,000 per month. You need capital quickly and you have been declined by traditional banks. The speed and flexible credit requirements represent genuine advantages for businesses that cannot access conventional financing.

However, you should calculate the true cost carefully. Remain aware of the data breach history and compare offers from multiple lenders before committing. If you can qualify for SBA loans or bank financing, those options will likely prove significantly cheaper over time.

Before applying

Verify you meet the $20,000 monthly revenue requirement consistently. Calculate the APR equivalent of any factor rate offered to understand the true cost of borrowing. Ensure your business can sustain daily or weekly payment withdrawals without creating cash flow problems.

Most importantly, obtain quotes from at least three lenders. This confirms you are receiving competitive terms for your specific situation.

Sponsored Advertising Content:

Advertorial or Sponsorship User published Content does not represent the views of the Company or any individual associated with the Company, and we do not control this Content. In no event shall you represent or suggest, directly or indirectly, the Company's endorsement of user published Content.

The company does not vouch for the accuracy or credibility of any user published Content on our Website and does not take any responsibility or assume any liability for any actions you may take as a result of reading user published Content on our Website.

Through your use of the Website and Services, you may be exposed to Content that you may find offensive, objectionable, harmful, inaccurate, or deceptive.

By using our Website, you assume all associated risks.This Website contains hyperlinks to other websites controlled by third parties. These links are provided solely as a convenience to you and do not imply endorsement by the Company of, or any affiliation with, or endorsement by, the owner of the linked website.

Company is not responsible for the contents or use of any linked website, or any consequence of making the link.

This content is provided by New Start Advantage LLC through a licensed media partnership with Inquirer.net. Inquirer.net does not endorse or verify partner content. All information is for educational purposes only and does not constitute financial advice. Offers and terms may change without notice.