Advertorial or Sponsorship User published Content does not represent the views of the Company or any individual associated with the Company, and we do not control this Content. In no event shall you represent or suggest, directly or indirectly, the Company's endorsement of user published Content.

The company does not vouch for the accuracy or credibility of any user published Content on our Website and does not take any responsibility or assume any liability for any actions you may take as a result of reading user published Content on our Website.

Through your use of the Website and Services, you may be exposed to Content that you may find offensive, objectionable, harmful, inaccurate, or deceptive.

By using our Website, you assume all associated risks.This Website contains hyperlinks to other websites controlled by third parties. These links are provided solely as a convenience to you and do not imply endorsement by the Company of, or any affiliation with, or endorsement by, the owner of the linked website.

Company is not responsible for the contents or use of any linked website, or any consequence of making the link.

Try Pennie Reviews and Ratings

Pennie Official Logo

Try Pennie advertises loans. What many applicants receive is a debt settlement program.

That gap is the most important thing to understand before you submit your information. Try Pennie is not a lender. It is a referral marketplace operated by Pennie Mgmt, LLC, founded in 2022, that distributes your application to a network of third-party lenders and debt relief companies. Borrowers with stronger credit may see loan offers. Those with lower scores are frequently routed to settlement options packaged under the “income-based consolidation” label, a product with a very different cost structure, credit impact, and timeline than a traditional loan.

This review covers how Try Pennie works, what it actually costs, what borrowers have reported on Trustpilot, Reddit, and the BBB, and what to consider before deciding whether to apply.

Evaluate these top-rated lenders to find a better match for your credit tier:

- Direct Lending Excellence: Matches you with the best loans.

- Loans ranging from $2,500 to $100,000

- Flexible terms: 3 to 120 months, 24 hours post-approval

- Same day approval

- Direct Lending Excellence: Matches you with the best loans with optimal loan terms.

- Comprehensive Loan Network: Loans ranging from $2,500 to $50,000

- Flexibility & Speed: Flexible terms from 3 to 120 months, 24 hours post-approval.

- Loan amounts up to $100,000

- Custom Terms: Repayment periods from 12 to 60 months with fast 48-hour approvals.

- Trusted Expertise: Recognized for ethical lending and innovative financial solutions.

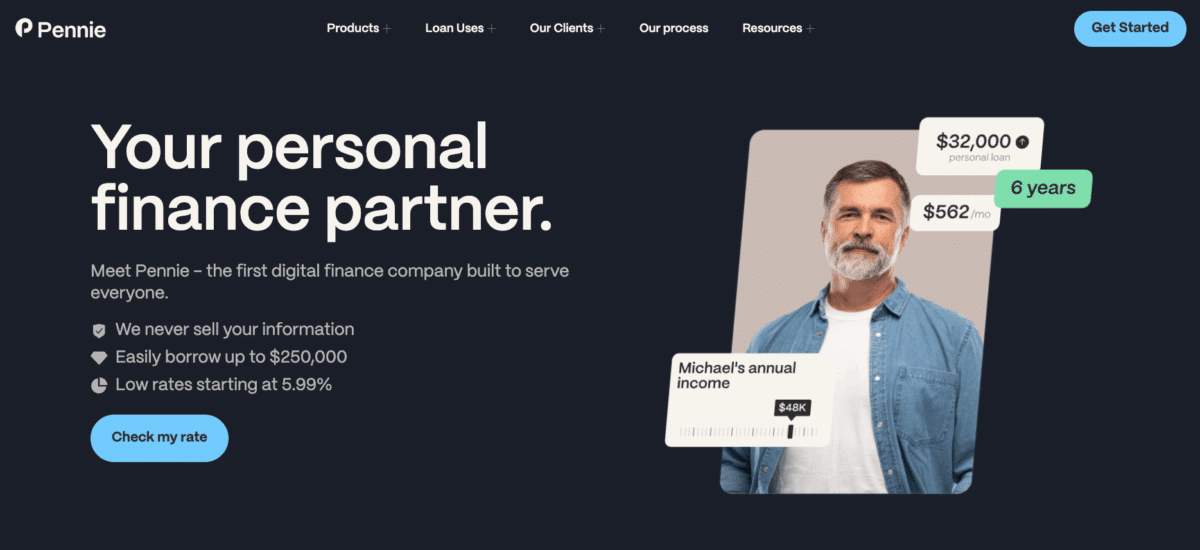

What is Try Pennie?

Pennie Official Website Homepage

Before we get into offerings and customer sentiment, let’s look into Try Pennie background:

Company overview and business model

Try Pennie (Pennie Mgmt, LLC) operates from Miami under CEO Sam Mkhitaryan. The company markets “income-based consolidation loans” and claims to have supported more than 32 million clients, along with $1B+ in credit products annually. These numbers represent inquiries and referral matches. They do not reflect loans funded by try pennie.

Try Pennie is not a lender. It is not BBB accredited, has no visible AFCC affiliation, and does not hold lender licenses. The platform markets nationwide. Actual service availability depends on your state and your assigned partner.

How Try Pennie works

The process begins with a quick online intake form. You enter personal details, income information, and debt amounts. A soft pull may be used initially. Later, partner lenders may run hard inquiries.

Try Pennie distributes your information to a network of lenders and debt settlement companies. You may receive loan offers if your profile qualifies. Many applicants receive debt settlement options instead. Settlement is often presented as “income-based consolidation.”

All final terms come from the partner provider. Try Pennie earns referral commissions, but the amounts are not disclosed publicly.

Is Try Pennie legit?

Try Pennie is a real company. It operates a functional referral marketplace. The concerns relate to clarity. Because the brand presents loan-style messaging but frequently delivers debt settlement outcomes, expectations can shift quickly. You should confirm all fees and risks directly with whichever partner ultimately handles your account.

State availability

Try Pennie markets its offerings nationally across the United States. The actual service you receive depends on your partner match and your state. Full availability is confirmed after submitting your information.

What are customers saying about Try Pennie?

Let’s look at what existing customers have to say about Try Pennie:

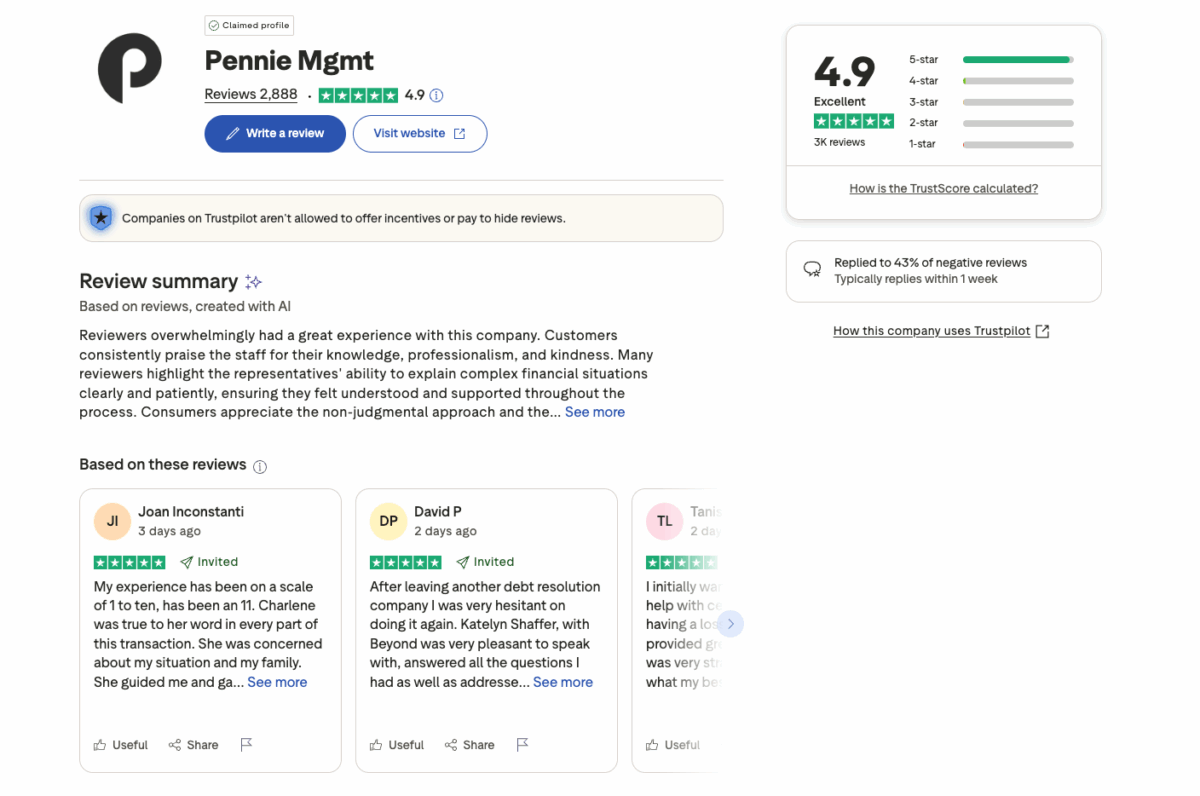

Trustpilot reviews

Pennie Mgmt Trustpilot Profile

Trustpilot displays ~2,500 reviews with ratings near 4.9–5.0 stars. Users frequently praise the empathy, patience, and clarity of customer representatives.

Highlighted quotes include:

- “John Kite was very patient and thorough. Even though I didn’t qualify for any loans I did qualify for Beyond…”

- “My experience was quite phenomenal with Marquise W. He was very detailed in providing me information…”

- “The customer service was excellent… The team went above and beyond…”

These reviews focus heavily on customer service. Some users mention confusion about loan options vs settlement, but these comments appear less frequently.

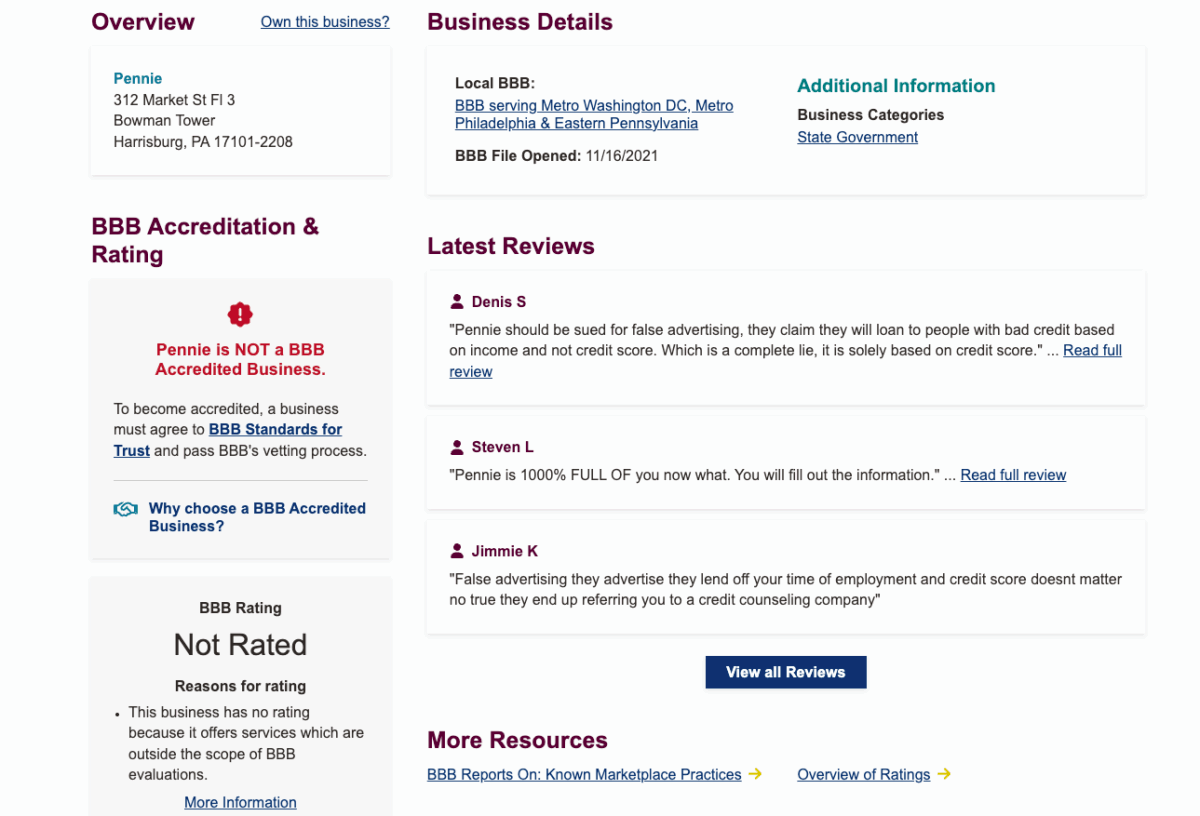

Better Business Bureau (BBB) reviews

Pennie BBB Business Profile

Try Pennie is not BBB accredited. Complaints describe unclear expectations, misleading advertising, and difficulty getting straight answers. Reviewers note that the platform presents itself like a lender but primarily routes users to settlement providers.

Reddit reviews

Reddit users communicate more bluntly:

- “They’re a debt settlement company. They don’t offer loans.”

- “Very dishonest… should be reported to SEC.”

- “Letters promising $25k or $50k loans only to be told they can only offer ‘debt relief’. Total BS.”

Users also mention persistent calling and pressure if they decline enrollment.

Authenticity assessment

Feedback is polarized. Trustpilot reviews highlight positive service experiences. Reddit and BBB focus on transparency issues and mismatches between advertising and reality. The overall pattern is clear. Many users expect loans but are instead presented with settlement programs.

What does Try Pennie offer?

The full offerings of Try Pennie may surprise you. Let’s take a look:

Personal loans (through partners)

Try Pennie can match applicants with third-party lenders offering personal and consolidation loans ranging from $1,000 to $250,000. APRs, loan terms, and origination fees are determined by the lender. Funding may take several days after approval. Hard credit pulls may occur.

Debt relief programs

Many users with lower credit profiles see settlement options instead of loans. Debt settlement involves stopping payments and allowing a negotiator to work with creditors. Fees are 15–25% of enrolled debt, charged after settlement agreements are reached. Settlement can damage your credit and increase collection activity.

What Try Pennie does not offer

try pennie does not offer tax relief, credit repair, or home loans. It focuses on referrals for loans and debt settlement services.

Eligibility and application process of Try Pennie

Here is everything you can expect when trying to apply to Try Pennie:

Minimum requirements

Users must be 18+. Eligibility depends on partner criteria. Lower-credit users commonly see settlement options instead of loans.

Required documentation

Documentation may include income verification, ID confirmation, bank statements, and creditor information.

Application timeline

Prequalification responses can appear within minutes. Loan matches may take minutes to 24 hours. Loan funding takes several days. Settlement outcomes take longer, often months, before the first negotiation occurs.

How much will Try Pennie actually cost?

We don’t want you to have any surprises when it comes to cost of using Try Pennie. Here is everything you can expect as far as costs and fees:

Fee types

Debt settlement programs charge 15–25% of enrolled debt. Fees are charged after settlements. Loan origination fees commonly fall between 1–6%, depending on the lender. Try Pennie receives referral commissions, which are not disclosed.

Pricing transparency

Transparency is limited. The website does not clearly distinguish loans from settlement programs. Many users discover fees and risks later in the process.

How is Try Pennie compared to other options?

The loan lender and debt relief scene is well saturated. Here is how Try Pennie stands in the field:

Direct lender alternatives

LendingClub, Discover, SoFi, and LightStream publish APR ranges and eligibility rules upfront. Underwriting is predictable.

Debt relief alternatives

Prominent settlement firms include National Debt Relief, Freedom Debt Relief, and Beyond Finance. They offer clearer fee disclosures and longer industry track records.

When competitors win

Direct lenders win on transparency and predictability. Debt relief companies win on clarity and published success metrics. Try Pennie appeals to users who want quick intake and supportive guidance.

Pros and cons of Try Pennie

Try Pennie is not a perfect service. Here is where it’s strong and where it lags behind:

Pros

- Fast intake

- Friendly representatives

- Multiple partner pathways

Cons

- Not a lender

- Limited transparency

- Aggressive follow-ups reported

- BBB and Reddit concerns

Who should (and shouldn’t) use Try Pennie

Try Pennie is certainly not for everyone. Here is an analysis of what the ideal candidate looks like, versus who would be best served to steer clear:

Ideal candidates

Try Pennie works best for consumers who want to explore multiple options quickly without committing upfront. If you’re someone who feels overwhelmed by debt and simply needs a starting point, the platform’s rapid outreach and supportive guidance can make the process feel less daunting. Users who appreciate having an empathetic representative walk them through their situation may also find Try Pennie appealing. The platform helps you understand your current financial position and gives you clarity around possible solutions, even if the actual offers come from third-party providers. Try Pennie can be useful if you’re open to both loan and settlement conversations and want to see which direction partners recommend based on your profile.

Not recommended for

Try Pennie is less ideal for users who want strict clarity on loan terms before engaging with a provider. If you already know you want a personal loan with specific APR ranges, and you want that information upfront, direct lenders offer a smoother and more transparent path. The platform also may not be a fit for users who cannot risk the credit consequences associated with debt settlement, as many applicants—especially those with lower credit—discover settlement is the primary solution offered. This shift can be surprising to users expecting consolidation loans and may lead to frustration if they were not prepared for that outcome. If you need absolute transparency from the first step, or if you want a highly predictable experience, Try Pennie may not be the right match.

Expert tips and success strategies for Try Pennie

Follow these rules of thumb to get the most out of Try Pennie:

Preparation checklist

Before starting your application, review your financial situation clearly. Know your total debt, minimum payments, and monthly income. Gather recent bank statements, pay stubs, and creditor information. This preparation helps ensure that whichever provider you’re matched with can evaluate your case accurately. It also helps you stay grounded and avoid being caught off guard by questions during the intake process. Preparing documents ahead of time allows you to compare offers more efficiently and makes it easier to spot inconsistencies or red flags.

Mistakes to avoid

Don’t assume that Try Pennie will present a loan option, even if that’s what the ad implied. Many users report that a conversation begins with the promise of consolidation but shifts toward settlement. Avoid agreeing to any program until you fully understand the terms. Don’t skip reading disclosures or rush through explanations. Don’t overlook the potential credit impact of settlement. Don’t allow pressure or urgency to dictate your decision. Keep asking questions until everything is clear, and ensure every promise made verbally is also provided in writing.

Strategies to maximize results

You’ll get the best outcome by comparing Try Pennie’s partner offers against direct lenders and established settlement firms. That comparison gives you perspective on pricing, timelines, and expectations. Ask for fee structures, settlement timelines, and credit pull information from each provider. Track names, dates, and details of every call. If something feels unclear, ask for verification in writing. The more information you gather, the more empowered you are. This approach also protects you from misunderstandings and ensures you make a fully informed choice that aligns with your goals.

Try Pennie customer service and support analysis

Here is a breakdown of what to expect from the customer service of Try Pennie:

Support channels

Try Pennie begins with an online intake system but quickly transitions to phone-based support. Users consistently mention speaking with representatives who are calm, patient, and thorough. This direct interaction can be comforting for applicants who feel overwhelmed by debt. Phone support makes the process feel personal, and many users note that representatives take time to explain their financial situations in detail.

Responsiveness

The platform responds quickly during the early stages. Many reviews mention immediate callbacks and efficient communication. This responsiveness helps set a positive tone up front, especially for users who feel anxious or stressed. But the quality of responsiveness may shift once you’re matched with a partner provider. Depending on the company you ultimately work with, communication styles and availability may differ. Once a partner takes over, the experience relies heavily on that partner’s internal structure and responsiveness.

Complaint resolution

This area is more mixed. Reddit and BBB reviews describe aggressive follow-ups and pressure to enroll. Some users report difficulty getting straight answers once they express hesitation or decline an offer. Complaint resolution can feel disjointed because try pennie itself is not the company servicing your program. Once you enter a partner’s system, you must deal with that provider directly. This layered approach can make it harder to resolve disputes or misunderstandings. For this reason, it’s essential to keep copies of disclosures, terms, and emails. Having everything documented protects you if questions or conflicts arise later.

Alternatives to Try Pennie

Consider these options before committing to Try Pennie:

Loan alternatives

If you want predictable loan options with clear APRs upfront, start with lenders like LendingClub, Discover, SoFi, or LightStream. These companies provide detailed information before you apply, including APR ranges, origination fees, and eligibility criteria. Their underwriting processes are consistent, and you can quickly assess whether a loan is realistic for your situation. This clarity eliminates surprises and helps you compare apples to apples across lenders.

Counseling alternatives

Nonprofit credit counseling agencies offer a very different kind of support. If you’re overwhelmed but still able to make monthly payments, a debt management plan (DMP) might be a safer path. DMPs typically reduce interest rates and consolidate payments into a single monthly contribution without stopping payments completely. This avoids the credit damage associated with settlement and reduces the likelihood of legal exposure. DMPs can also offer educational guidance and ongoing accountability.

Settlement alternatives

If you are considering debt settlement, look at established providers such as National Debt Relief, Freedom Debt Relief, or Beyond Finance. These companies have clearer fee disclosures, longer histories, and more detailed published information about timelines and client outcomes. While settlement still carries risks in general, these brands offer a more transparent experience than many lead-generation platforms. Comparing multiple settlement providers helps you understand fee structure, communication style, and what success looks like across the industry.

Try Pennie Frequently Asked Questions

Is Try Pennie a lender?

No. Try Pennie is a referral marketplace.

Is Try Pennie legit?

Yes, but transparency concerns exist.

What fees does Try Pennie charge?

Fees come from partner providers, not from try pennie directly.

How does Try Pennie affect credit?

Hard pulls can happen. Settlement programs damage credit.

How fast is the process?

Prequal is fast. Loan funding takes days. Settlement takes months.

Does Try Pennie share information?

Yes. Information is shared with partners and affiliates.

Are there any regulatory actions?

No direct actions as of 2025. Similar patterns are warned about by regulators.

Where is Try Pennie available?

Availability varies by state and partner.

Final verdict: Is Try Pennie actually worth it?

Let’s do a final assessment of Try Pennie:

Summary assessment

Try Pennie delivers fast intake and empathetic support, which can feel reassuring when you’re stressed. The representatives are consistently praised for their patience, clarity, and tone. However, the platform’s lack of transparency matters. Many users expect a loan and instead receive settlement discussions. For this reason, you should approach Try Pennie as a referral service rather than a direct lender.

Best use cases

Try Pennie can be helpful if you’re starting your research and want to explore several options quickly. It offers a straightforward intake and immediate human interaction. If you want guidance and a chance to talk through your situation with a calm representative, the platform delivers that experience reliably. It’s also useful for people who are open to either loans or settlement and want to hear professionals’ recommendations.

When to avoid Try Pennie

Avoid Try Pennie if you want total clarity prior to applying. If you prefer to know your APR range, fee structure, and loan terms upfront, direct lenders offer a better experience. If settlement is not an option you’re open to—or if you cannot commit to the credit impacts and potential legal exposure—it’s better to pursue other solutions. If transparency is your priority, look for providers that publish detailed information from the beginning.

Additional resources for Try Pennie

Official sources

trypennie.com and partner disclosures

Consumer education

CFPB and FTC guides on debt relief and consolidation

Helpful tools

Nonprofit counseling directories and reputable lenders

Sponsored Advertising Content:

Advertorial or Sponsorship User published Content does not represent the views of the Company or any individual associated with the Company, and we do not control this Content. In no event shall you represent or suggest, directly or indirectly, the Company's endorsement of user published Content.

The company does not vouch for the accuracy or credibility of any user published Content on our Website and does not take any responsibility or assume any liability for any actions you may take as a result of reading user published Content on our Website.

Through your use of the Website and Services, you may be exposed to Content that you may find offensive, objectionable, harmful, inaccurate, or deceptive.

By using our Website, you assume all associated risks.This Website contains hyperlinks to other websites controlled by third parties. These links are provided solely as a convenience to you and do not imply endorsement by the Company of, or any affiliation with, or endorsement by, the owner of the linked website.

Company is not responsible for the contents or use of any linked website, or any consequence of making the link.

This content is provided by New Start Advantage LLC through a licensed media partnership with Inquirer.net. Inquirer.net does not endorse or verify partner content. All information is for educational purposes only and does not constitute financial advice. Offers and terms may change without notice.