Advertorial or Sponsorship User published Content does not represent the views of the Company or any individual associated with the Company, and we do not control this Content. In no event shall you represent or suggest, directly or indirectly, the Company's endorsement of user published Content.

The company does not vouch for the accuracy or credibility of any user published Content on our Website and does not take any responsibility or assume any liability for any actions you may take as a result of reading user published Content on our Website.

Through your use of the Website and Services, you may be exposed to Content that you may find offensive, objectionable, harmful, inaccurate, or deceptive.

By using our Website, you assume all associated risks.This Website contains hyperlinks to other websites controlled by third parties. These links are provided solely as a convenience to you and do not imply endorsement by the Company of, or any affiliation with, or endorsement by, the owner of the linked website.

Company is not responsible for the contents or use of any linked website, or any consequence of making the link.

Enable Loans Reviews and Ratings

Enable Loans Logo

The bank said no. The credit card is maxed. The next paycheck is days away. That is the moment Enable Loans appears in search results, promising same-day cash, no hard credit check, instant approval. It sounds like a lifeline.

But borrowers deserve the full picture before filling out that application. This Enable Loans review covers what the company is, how tribal lending actually works, what a loan genuinely costs, and what real customers are saying.

Read on to decide whether Enable Loans is the right move or whether a safer option is within reach.

TL;DR: Enable Loans (2026) quick summary

- Extreme Cost: Charges 600%–723% APR; borrowing $500 can cost over $1,100 to repay.

- Tribal Status: Operates under tribal law, meaning state interest rate caps and consumer protections do not apply.

- Poor Reputation: 1-star rating on BBB and Trustpilot with 119+ complaints regarding unauthorized withdrawals and poor support.

- Fast Access: No hard credit check and same-day funding available, making it accessible but dangerous.

- Availability: Prohibited in 14 states (including NY, PA, IL, and GA).

- Verdict: Last resort only. If used, repay within 30 days to avoid massive interest.

Evaluate these top-rated lenders to find a better match for your credit tier:

- Direct Lending Excellence: Matches you with the best loans.

- Loans ranging from $2,500 to $100,000

- Flexible terms: 3 to 120 months, 24 hours post-approval

- Same day approval

- Direct Lending Excellence: Matches you with the best loans with optimal loan terms.

- Comprehensive Loan Network: Loans ranging from $2,500 to $50,000

- Flexibility & Speed: Flexible terms from 3 to 120 months, 24 hours post-approval.

- Your Best Lending Partner: Rated #1 for customer satisfaction and personalized service.

- Fast, Easy Approvals: Get funded in as little as 24 hours with zero hidden fees.

- Tailored Loan Solutions: Flexible terms designed around your financial goals.

What is Enable Loans?

Enable Loans Website Homepage

Enable Loans is the consumer lending arm of Wakpamni Lake Community Corporation (WLCC). This is a tribal entity organized under the Oglala Sioux Tribe of the Pine Ridge Reservation in South Dakota.

It is not a state-licensed lender. It operates under Consumer Loan License No. FS-51, issued in May 2024 under the tribe’s own Tribal Consumer Financial Services Regulatory Code.

The company’s mailing address is in Solon, Iowa. Its physical lending headquarters sits on tribal land at 1 Wakpamni Lake Road, Wakpamni Lake, South Dakota. All lending operations fall under tribal jurisdiction.

Enable Loans was established partly to support economic development for the Pine Ridge community. That community is one of the most economically distressed regions in the United States. Poverty rates exceed 50 percent. Unemployment surpasses 80 percent.

What ‘tribal lender’ means for borrowers

Tribal lenders operate on sovereign tribal land under their own governing codes. This matters a great deal for borrowers.

State interest rate caps and consumer lending statutes generally do not apply to tribal lenders. A state might cap APRs at 36 percent or ban certain high-cost loan structures altogether. Enable Loans is not bound by those rules.

In practical terms, this creates two outcomes. First, borrowers rejected by regulated lenders can still get approved. Second, if something goes wrong, unauthorized withdrawals, billing errors, or account disputes, the borrower’s legal recourse is limited to the tribe’s own complaint process, not state courts.

Enable Loans is a legal tribal lender charging 600–723% APR on loans of $500–$2,000. It has a 1-star BBB rating, 119+ complaints, and limited consumer protections. Use only as a last resort if you can repay within one or two billing cycles.

Enable Loans state availability

Enable Loans does not operate in 14 states and territories: Arkansas, the District of Columbia, Georgia, Illinois, Massachusetts, Maryland, Minnesota, New York, Pennsylvania, Puerto Rico, South Dakota, Virginia, the U.S. Virgin Islands, and West Virginia.

Notably, the lender does not serve South Dakota, the very state where its tribal land and lending headquarters are located.

What Enable Loans actually offers

Enable Loans offers one product: short-term personal installment loans.

Enable Loans loan amounts and terms

There are no auto loans, credit lines or refinance products.

- Loan amounts: $500 to $700 for first-time borrowers; up to $2,000 for returning borrowers

- Repayment terms: Two to six months, with weekly, biweekly or monthly payment schedules

- Credit check: No hard credit pull; verification uses soft checks via Clarity, DataX, Factor Trust, Experian, Equifax and TransUnion

- Collateral: None required

- Funding method: Real-Time Payments (RTP) immediately after approval; Automated Clearing House (ACH) transfer if RTP is unavailable at the borrower’s bank

No prepayment penalty applies. Borrowers who pay off early may qualify for a small interest discount.

Enable Loans application process

The application is entirely online and takes three steps. First, fill out a short form with basic personal and financial details. Second, receive an automated real-time decision. Third, e-sign the loan agreement if approved.

Same-day funding is available for borrowers approved before 11:30 a.m. CST on a business day whose bank supports RTP. Otherwise, funds arrive by the next business day via ACH.

Customer service is available by phone at 1 (888) 704-3223, Monday through Friday, 8 a.m. to 11 p.m. ET.

Enable Loans eligibility requirements

To qualify, applicants must meet all of the following:

- Be at least 18 years old

- Be a U.S. citizen or legal permanent resident

- Not be active duty military, a military spouse or a dependent

- Have a regular, verifiable income

- Hold an active checking account with a valid debit card

- Have a valid email address and cell phone number

- Reside in a state where Enable Loans operates

No minimum credit score is required. Enable Loans accepts applicants rejected by banks and traditional lenders.

How much does Enable Loans actually cost?

This is the section most borrowers skip until it is too late. Read it carefully.

Enable Loans interest rates, and APR explained

Enable Loans charges an APR between 600 percent and 723.01 percent. That figure depends on the loan amount and the repayment schedule chosen.

To put those numbers in context:

- Payday loans typically carry APRs between 300 and 400 percent

- Other tribal lenders typically range from 440 to 700 percent APR

- Regulated bad-credit personal lenders such as Avant, OppLoans and OneMain Financial charge APRs of 18 to 35.99 percent

- Federal credit union payday alternative loans (PALs) are capped at 28 percent APR by law

Enable Loans sits at the extreme high end, even by tribal lending standards.

Enable Loans fee breakdown

- Late payment fee: $35 if payment is more than seven days late

- Returned payment fee: $30

- Origination fee: May apply, confirm against the loan agreement before signing

- Application fee: None

- Prepayment penalty: None; early payoff may reduce total interest paid

What a $500 Enable Loan actually costs

Here is a concrete repayment scenario using Enable Loans’ published rate:

- Loan amount: $500

- APR: 723.01 percent

- Repayment structure: Biweekly payments over approximately five months

- Total amount repaid: $1,112.45

- Total interest paid: $612.45

- Real-world complaint example: one borrower reported biweekly payments of $429 on a $750 loan at 673 percent APR (sourced from BBB complaint records)

- Comparison benchmark: a $500 personal loan through a regulated lender at 35.99 percent APR would cost approximately $545 total, a difference of over $560

Borrowing $1,000 at 723 percent APR results in a total repayment of approximately $2,281.28. That is over $1,281 in interest alone. By comparison, a $500 personal loan through a regulated lender at 35.99 percent APR costs roughly $545 total. The difference is more than $560 on the same $500 borrowed.

Always read the full repayment schedule before accepting any loan offer. Many borrowers report not understanding the total cost until after signing.

Enable Loans cost compared to other lenders

Enable Loans is not just expensive by conventional standards. It is expensive by tribal lending standards.

- Payday loans: 300 to 400 percent APR

- Other tribal lenders: 440 to 700 percent APR

- Enable Loans: 600 to 723 percent APR, among the highest of any legal lender

- Regulated bad-credit lenders: 18 to 35.99 percent APR

- Federal credit union PALs: capped at 28 percent APR

Enable Loans customer reviews and complaints

A lender’s legitimacy is best measured by its track record, and for Enable Loans, that record is defined by a high volume of consumer complaints and technical failures.

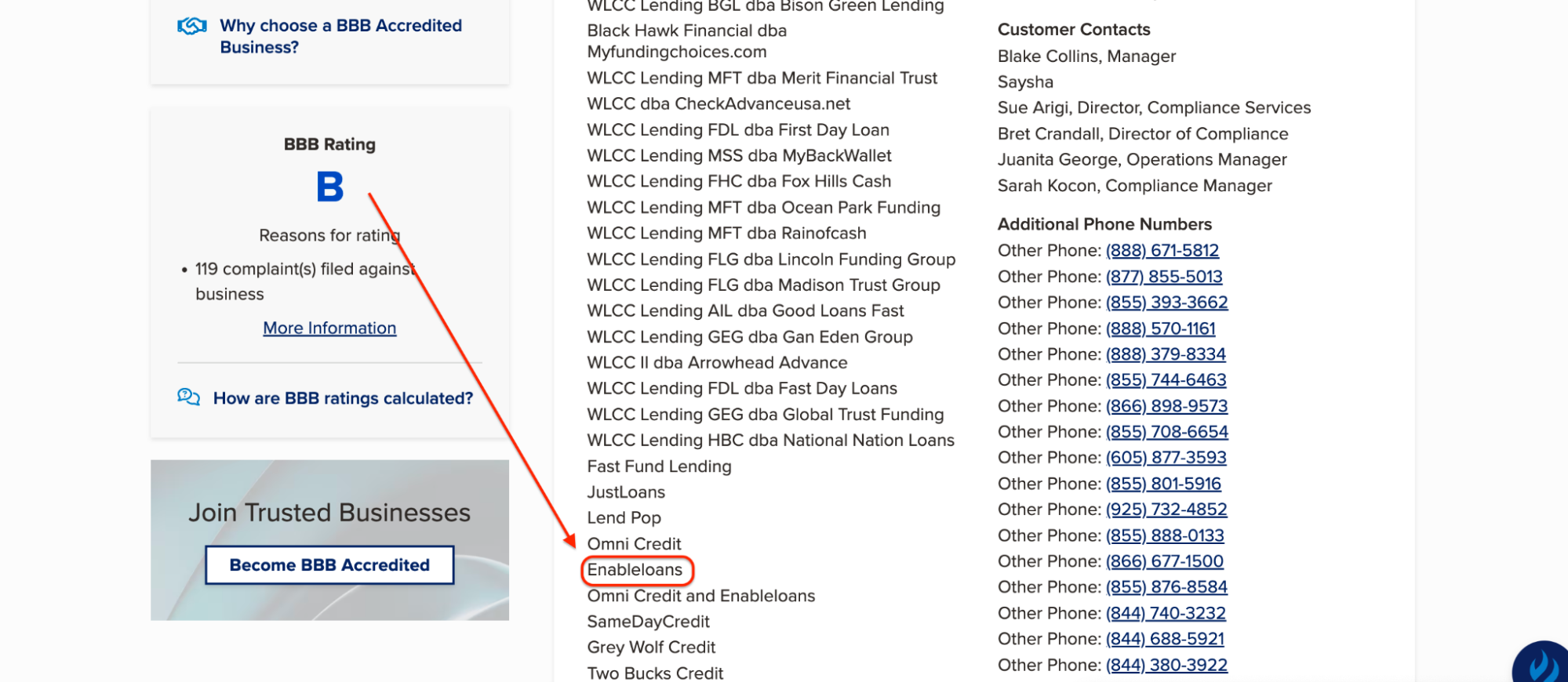

Better Business Bureau (BBB) reviews

Enable Loans BBB profile

Over 119 BBB complaints have been filed in the past three years. The parent company WLCC holds a B rating for responding to complaints but carries a 1-star customer review average.

WLCC holds a B rating from the BBB for responding to complaints, but that rating reflects complaint response, not customer satisfaction. The company is not BBB accredited.

Recurring themes across complaint records include:

- Server outages are causing funding delays while interest continues to accrue

- ACH withdrawals continue after accounts show as paid or closed

- Difficulty reaching live customer service representatives

- Overdrafts caused by incorrectly timed or unexpected withdrawals

- Inability to close accounts or receive written payoff confirmation

WLCC is also listed under nearly 100 alternate business names on the BBB website. That is a transparency concern worth noting before applying.

Trustpilot reviews

Enable Loans Trustpilot profile

Enable Loans has a Trustpilot profile with seven reviews and a score of 2.3 out of 5. All seven reviews are 1-star ratings.

Recurring issues reported on Trustpilot include loan offers being reduced after initial approval, persistent website and login errors, and difficulty reaching a live agent. One reviewer reported being approved for $1,000, then revised to $300, then to $100- and never receiving the funds due to login errors.

Another reviewer described taking out a loan, paying it off quickly and then being denied as a returning borrower with no explanation. No positive reviews appear in the current record.

Reddit Reviews

The Truth About Enable Loans Lender – Must Watch For Those Of You Considering Borrowing Money There! byu/HopeItHelpsYoutube inIssuesResolving

Enable Loans is grouped with other tribal lenders in Reddit threads focused on high-cost emergency borrowing. The most consistent advice: pay off as fast as possible. Compounding interest makes longer repayment terms significantly more expensive.

Some Reddit users have noted that tribal lenders may not be able to pursue borrowers in state court due to sovereign immunity. However, that does not prevent aggressive ACH withdrawal attempts or third-party collection activity.

Enable Loans outcomes and success rate

Enable Loans does not publish approval rate data, borrower success statistics or default figures.

Same-day funding is conditionally available. The condition: approved before 11:30 a.m. CST, and the borrower’s bank must support RTP. In all other cases, funds arrive the next business day via ACH.

Enable Loans states on its own website that its loans have a high APR and should not be used as a long-term financial solution. There is no evidence from public reviews of meaningful customer loyalty or long-term positive financial outcomes.

Most borrowers who leave reviews describe one of two outcomes: paying off the debt as fast as possible, or becoming trapped in a repayment cycle. The best-case scenario is borrowing the minimum needed and clearing the balance within the first or second billing cycle.

For general strategies on paying down high-interest debt quickly, these debt payoff tactics apply equally well to short-term loans like this one.

Enable Loans pros and cons

Below is a detailed look at why Enable Loans is accessible to many but remains a high-risk financial move.

Pros

- No hard credit check; no minimum credit score

- Fast, fully online application with a real-time decision

- Same-day funding via RTP when eligible

- No prepayment penalty; early payoff discounts may apply

- Accessible to borrowers rejected by mainstream lenders

Cons

- APR of 600 to 723 percent, among the most expensive legal loan products available

- 1-star customer rating on both BBB and Trustpilot

- More than 119 BBB complaints in three years

- Tribal sovereign immunity significantly limits borrowers’ legal recourse

- Not licensed in any U.S. state; flagged by multiple state regulators, including Washington DFI (February 2026, names Enable Loans specifically)

- Recurring reports of technical failures, unauthorized withdrawals and unresponsive support

- Not available in 14 states and territories

- Origination fees may apply. Confirm before signing

Who Enable Loans is best for

Here is a breakdown of who might benefit from this speed and who should stay far away.

Best for

- Borrowers with very poor or no credit who have exhausted all regulated alternatives

- People who need $500 or less in a genuine emergency and can repay within 30 days

- Individuals in eligible states who fully understand the risks of tribal lending

Not recommended for

- Anyone who qualifies for a credit union PAL, online installment loan, or cash advance app

- Borrowers in restricted states, including New York, Pennsylvania, Virginia, Massachusetts and Illinois

- Active military service members, tribal lenders may not honor the Military Lending Act rate caps

- Anyone who cannot pay off the loan quickly, the longer it runs, the worse the math becomes

Better alternatives to Enable Loans

For most borrowers considering Enable Loans, a safer and significantly cheaper option exists. Work through these categories before submitting an application.

Regulated online lenders for bad credit

OppLoans, Avant, Upstart and OneMain Financial offer personal installment loans to borrowers with credit scores from 500 to 580. APRs typically run between 18 and 35.99 percent. OppLoans also reports payments to all three major credit bureaus, a meaningful advantage for anyone trying to rebuild credit while managing debt.

Credit union payday alternative loans

Federal credit unions offer PALs with amounts up to $2,000, repayment terms of one to 12 months and interest capped at 28 percent APR by federal law.

Two types exist. PAL I requires 30 days of membership before applying. PAL II has no waiting period. Many credit unions are open to anyone based on employer, location or community association.

Cash advance apps

Apps such as EarnIn, Brigit, Dave, and Chime SpotMe let borrowers access a portion of their next paycheck with zero or minimal interest. New user advances are typically $50 to $150. That limits their usefulness for larger emergencies, but for smaller cash gaps, they cost far less than any tribal loan product. For borrowers who need a larger regulated installment loan, NetCredit is one option worth comparing. Its APRs are high, but still well below Enable Loans’ range.

Nonprofit and community lending programs

Mission Asset Fund and similar organizations offer zero-interest lending circles. Dialing 211 connects borrowers to local groups that assist with rent, utilities, and groceries, without any debt at all.

These programs are widely underused. Exhausting them before taking on a 723 percent APR loan could save hundreds of dollars. Borrowers who want to compare other high-cost lenders side by side can also read this in-depth breakdown of Echo Credit another tribal-style lender with a similar cost structure.

Final verdict: Is Enable Loans worth it?

Enable Loans is technically legal, genuinely fast, and accessible to borrowers with poor credit. Those qualities are real.

The BBB complaint record, state regulatory alerts (including Washington DFI’s February 2026 alert naming Enable Loans specifically), 1-star Trustpilot rating, and reports of continued ACH withdrawals after payoff are compounding warning signs.

The BBB complaint record, state regulatory alerts, 1-star Trustpilot rating, and reports of continued ACH withdrawals after payoff are compounding warning signs.

Enable Loans is a last resort, and only for borrowers who are certain they can repay within one or two billing cycles. Before reaching that point, exhaust the safer options above. Credit union PALs, regulated online lenders, and cash advance apps can all meet the same emergency need at a fraction of the cost, with full consumer protections in place. Borrowers with a trusted family member or friend may also want to explore cosigner-based options like Transform Credit, a legitimate path to lower rates for those who qualify.

If Enable Loans remains the only viable path, borrow the smallest amount possible, pay it off as quickly as possible, and monitor bank statements closely for any unauthorized withdrawals after the balance is cleared.

Frequently asked questions about Enable Loans

Is Enable Loans a scam?

Enable Loans is not a scam in the legal sense. It is licensed under tribal law with disclosed rates and terms. However, its APR of 600 to 723 percent, combined with limited state oversight and more than 119 BBB complaints, leads many borrowers and financial advocates to describe its products as predatory. Legally operating and practically harmful are not mutually exclusive.

Is Enable Loans legit?

Yes, Enable Loans is a legitimate, operating lender. It is a subsidiary of WLCC, a real tribal entity on the Pine Ridge Reservation. It funds real loans. The legitimacy concern is not whether it operates; it does, but whether the cost structure is manageable for most borrowers. At 723 percent APR, it typically is not.

Does Enable Loans report to credit bureaus?

Enable Loans does not typically report payment activity to Equifax, Experian, or TransUnion. On-time payments will not help build or repair a credit score. However, a default may still be sold to a collection agency, which can result in a negative mark on a credit report.

Can Enable Loans sue borrowers who do not pay?

Due to tribal sovereign immunity, Enable Loans generally cannot pursue borrowers in state courts. However, it may continue ACH withdrawal attempts, refer accounts to third-party collectors, and contact borrowers by phone or mail. Stopping payment does not eliminate collection pressure.

What states is Enable Loans available in?

Enable Loans does not operate in Arkansas, the District of Columbia, Georgia, Illinois, Massachusetts, Maryland, Minnesota, New York, Pennsylvania, Puerto Rico, South Dakota, Virginia, the U.S. Virgin Islands, or West Virginia. Borrowers in all other U.S. states may be eligible, subject to the lender’s approval criteria.

Sponsored Advertising Content:

Advertorial or Sponsorship User published Content does not represent the views of the Company or any individual associated with the Company, and we do not control this Content. In no event shall you represent or suggest, directly or indirectly, the Company's endorsement of user published Content.

The company does not vouch for the accuracy or credibility of any user published Content on our Website and does not take any responsibility or assume any liability for any actions you may take as a result of reading user published Content on our Website.

Through your use of the Website and Services, you may be exposed to Content that you may find offensive, objectionable, harmful, inaccurate, or deceptive.

By using our Website, you assume all associated risks.This Website contains hyperlinks to other websites controlled by third parties. These links are provided solely as a convenience to you and do not imply endorsement by the Company of, or any affiliation with, or endorsement by, the owner of the linked website.

Company is not responsible for the contents or use of any linked website, or any consequence of making the link.

This content is provided by New Start Advantage LLC through a licensed media partnership with Inquirer.net. Inquirer.net does not endorse or verify partner content. All information is for educational purposes only and does not constitute financial advice. Offers and terms may change without notice.