Advertorial or Sponsorship User published Content does not represent the views of the Company or any individual associated with the Company, and we do not control this Content. In no event shall you represent or suggest, directly or indirectly, the Company's endorsement of user published Content.

The company does not vouch for the accuracy or credibility of any user published Content on our Website and does not take any responsibility or assume any liability for any actions you may take as a result of reading user published Content on our Website.

Through your use of the Website and Services, you may be exposed to Content that you may find offensive, objectionable, harmful, inaccurate, or deceptive.

By using our Website, you assume all associated risks.This Website contains hyperlinks to other websites controlled by third parties. These links are provided solely as a convenience to you and do not imply endorsement by the Company of, or any affiliation with, or endorsement by, the owner of the linked website.

Company is not responsible for the contents or use of any linked website, or any consequence of making the link.

Tomo Mortgage Reviews and Ratings

Tomo Mortgage logo

Tomo Mortgage is a legitimate online lender built for home buyers. It posts real rates on its site. It charges no lender fees. And it closes 98 percent of its loans on time, by its own count. That makes it a strong pick for buyers who want to see a rate before they talk to anyone.

Its main claim is that its rates run about 0.5 percent below the market. No outside source proves that number. So buyers should still check it against a live quote. This review breaks down how the pricing works, what TrueRate does, what buyers say on Zillow and Reddit, and who the lender fits best.

Evaluate these top-rated lenders to find a better match for your credit tier:

- Direct Lending Excellence: Matches you with the best loans.

- Loans ranging from $2,500 to $100,000

- Flexible terms: 3 to 120 months, 24 hours post-approval

- Same day approval

- Direct Lending Excellence: Matches you with the best loans with optimal loan terms.

- Comprehensive Loan Network: Loans ranging from $2,500 to $50,000

- Flexibility & Speed: Flexible terms from 3 to 120 months, 24 hours post-approval.

- Loan amounts up to $100,000

- Custom Terms: Repayment periods from 12 to 60 months with fast 48-hour approvals.

- Trusted Expertise: Recognized for ethical lending and innovative financial solutions.

What is Tomo Mortgage?

Tomo Mortgage homepage

Tomo Mortgage is an online-only home loan company. It launched in 2020. A former Zillow executive, Greg Schwartz, co-founded it. Investors include Progressive Insurance, Ribbit Capital, DST Global, and NFX. The company has funded more than $3 billion in loans.

Tomo works as a licensed mortgage broker. It partners with established lenders to fund each loan. Its Nationwide Multistate Licensing System (NMLS) ID is 2059741. The main office sits in New York City. Bankrate named it a Best Online Lender for 2026.

The company focuses on home purchases, not refinances. It posts its rates online so buyers can compare before they apply. It also skips lender fees, which we cover below. One more feature stands out. Its TrueRate tool will even show a better rate at another lender if Tomo cannot win the deal.

Tomo Mortgage rates and fees, how the pricing model works

This is the heart of the review. The Reddit thread that ranks first for this brand is from loan officers, not buyers. They wanted to understand Tomo’s pricing. So buyers deserve a clear answer too.

Published rates and the no rate-keeping model

Tomo posts its mortgage rates right on its website. Most lenders hide rates behind a sales call. Tomo does not. Rate keeping is when a lender pads the rate it shows to lift its own profit. Tomo says it skips that markup and passes wholesale pricing straight to buyers. The company says its rates run about 0.5 percent below the market. It claims a full 1 percent below some big lenders.

Real quotes back this up in some cases. One buyer in Raleigh, North Carolina shared a 5.99 percent rate on a 30-year fixed loan with zero points and zero origination fees. Another buyer compared a local lender at 6 percent plus $1,595 in fees against Tomo at 5.625 percent with no fees.

Still, the edge is not a sure thing. One outside review found Tomo’s 2024 rates landed close to the market average, not far below it. So the smart move is simple. Pull a Tomo quote and compare it to two or three other lenders on the same day.

No lender fees, what this means and what it does not

Tomo charges no origination, processing, or underwriting fees. It guarantees $0 in lender fees. Most large lenders charge a median origination fee of about $1,360 on a 30-year conventional loan. Some charge far more.

No lender fees does not mean no closing costs. Third-party costs still apply. These include title insurance, appraisal, and government recording fees. On a $400,000 loan, total closing costs often run $8,000 to $12,000. Tomo’s share of that bill is zero, but the rest is not. The savings come from two places. The zero lender fees cut the upfront cost. The lower rate trims the monthly payment over the life of the loan. Many buyers report saving close to $15,000 in total loan cost versus other quotes.

What the Reddit loan officer thread says about Tomo’s pricing

The top result for tomo mortgage reviews is a Reddit thread in r/loanoriginators. It is titled “Tomo Mortgage Pricing..WOW.” The posters are loan officers, not buyers.

One officer wrote that Tomo beat his pricing by a wide margin, even on investment property. He saw rates 0.5 to 0.75 percent better than the market. He could not figure out how they did it. The thread reads as surprise at the low pricing, not a warning about fraud. That is a useful signal for buyers.

TrueRate, Tomo’s rate transparency tool

TrueRate is Tomo’s most unusual feature. It is a free AI tool. It uses real loan data to show a fair rate for each buyer’s profile. It shows what counts as a low, average, or high rate right now.

It also names lenders likely to offer each rate range, even when that lender is not Tomo. Lenders cannot pay to rank higher on it. The tool bases its math on the buyer’s location, home price, down payment, and credit score. It won a banking innovation award in 2025.

Tomo Mortgage at a glance

- Online mortgage lender for home purchases

- NMLS ID 2059741

- Founded in 2020 and based in New York City

- Available in more than 40 states and Washington, D.C.

- Loan types include conventional, Federal Housing Administration (FHA), Department of Veterans Affairs (VA), and jumbo purchase loans

- No U.S. Department of Agriculture (USDA) loans and no home equity products

- Minimum down payment of 3 percent for conventional, 3.5 percent for FHA, and zero for VA

- Minimum credit score around 580 for conventional loans

- Lender fees of $0, guaranteed

- Rate claim of about 0.5 percent below the market

- On-time closing rate of 98 percent, by company count

- Average time to close of about 25 days

- Rate lock of 30 days, with a price-match guarantee

- TrueRate tool for free rate comparison across lenders

- Trustpilot 4.5, Zillow about 4.6, Bankrate 4.9, ConsumerAffairs about 4.7

- Phone (737) 510-2523

Tomo Mortgage loan options

Tomo offers a focused set of purchase loans.

- Conventional loans need as little as 3 percent down. They suit buyers with steady credit.

- FHA loans need 3.5 percent down and a credit score of 580 or higher. They fit buyers with lower credit.

- VA loans need zero down for eligible service members and veterans.

- Jumbo loans cover homes priced above standard loan limits.

Tomo’s FHA loans allow a debt-to-income (DTI) ratio as high as 57 percent. That helps buyers who carry more monthly debt. These loans cover primary homes only, not investment property. Most Tomo loans need a credit score near 580, though the best rates go to scores of 700 or higher.

Tomo does not offer USDA loans. It does not offer home equity products. It offers refinancing only to current customers. It also runs a down payment help program in Connecticut, with plans to expand.

Tomo Mortgage on-time closing record

Tomo says it closes 98 percent of its loans on time. It compares that to a 40 percent industry average. The company says it hits this mark by automating much of the back-office work. Its average time to close is about 25 days, faster than many rivals.

Treat the 98 percent as a company figure, not an audited one. Still, buyer reviews back up the speed. Many say their loan closed on time. A few report delays, which we cover next. In a tight market, a fast and reliable close can win the deal. Tomo also backs its pricing with a price-match guarantee. It supports e-closings and remote online notarization, which can speed up signing day.

Tomo Mortgage reviews and ratings by platform

Tomo earns strong scores on most review sites. Here is how it stacks up as of June 2026. Across every platform, two themes repeat. Buyers praise the low rates and the zero lender fees. The main gripe is uneven communication during underwriting. Both themes are worth keeping in mind below.

Zillow reviews

Tomo Mortgage Zillow profile showing a 4.59 rating

Tomo holds about 4.6 stars on Zillow across roughly 84 reviews as of June 2026. Reviews there come from buyers who finished a loan, so they carry weight. Many praise low rates, waived appraisals, and clear updates. One buyer, GrecoISU, closed in February 2026, got a lower rate than local banks, and saved on a waived appraisal. Not every review is glowing. One buyer, Luis from Addison, Texas, reported poor communication and last-minute document requests that delayed the closing. Another buyer, Scott Chauncey, said Tomo would not give him a Loan Estimate and offered shifting answers. So service can vary by loan officer.

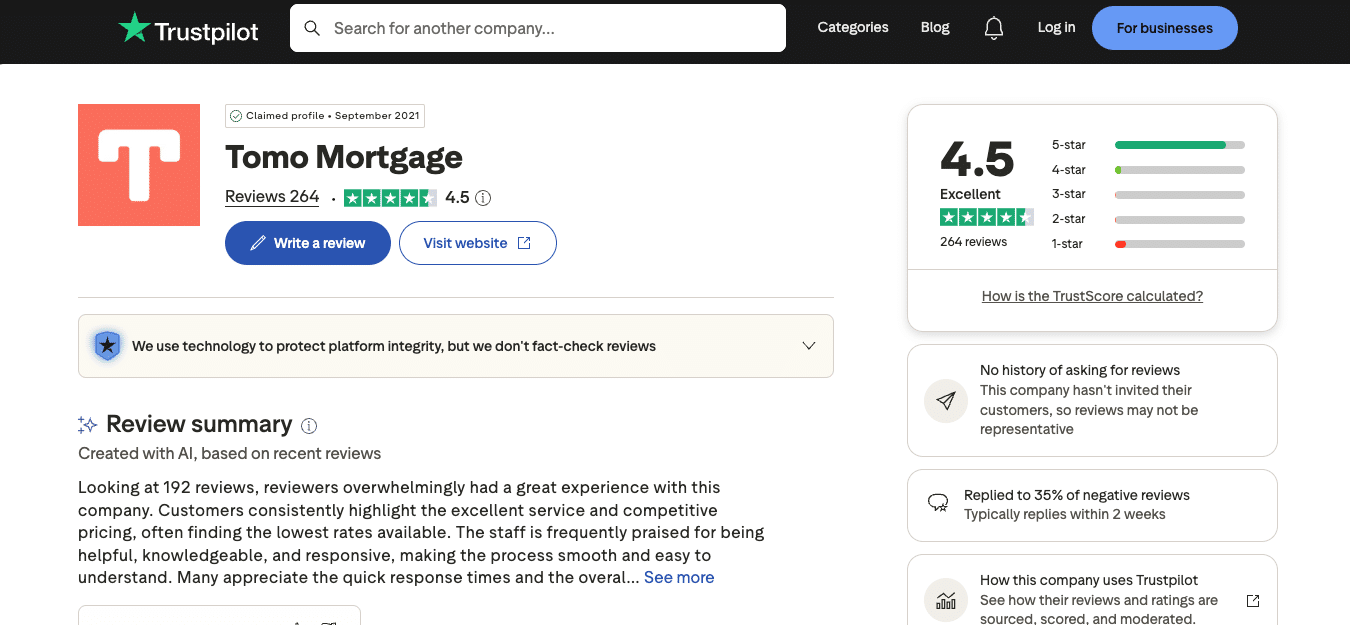

Trustpilot reviews

Tomo trustpilot profile

Tomo holds a 4.5-star rating on Trustpilot across 264 reviews as of June 2026. That puts it in the Excellent band. Recent reviewers in mid-2026 praise the lowest rates they could find, a smooth application, and loan officers who call and text after hours. Many name their loan officer in the review. The most common complaint is a closing delay or slow replies during underwriting.

Better Business Bureau (BBB) reviews

Tomo Mortgage is not accredited by the Better Business Bureau, and it had not earned a BBB rating as of June 2026. As a young company, it has a short BBB track record. Buyers who value a long BBB history should note this. A lack of accreditation is not a red flag on its own, but it is worth knowing. Note that a separate firm called TomoCredit is unrelated to Tomo Mortgage, so its BBB record should not be confused with the lender.

Reddit reviews

Reddit views are mixed but lean positive. In r/Mortgages, buyers call Tomo a legit lender with low rates and low fees, though several ask whether the pricing is too good to be true. The common worry is slow communication and uneven service. One buyer in r/HomeLoans saved about $15,000 in total loan cost versus another quote. He noted that replies were slow and that Tomo sold his loan to another servicer such as Pennymac soon after closing. A first-time buyer in r/FirstTimeHomeBuyer beat a Rocket quote by 0.5 percent with no lender fees, but had to re-upload documents during underwriting. Not every story is positive. One borrower in r/Mortgages reported that Tomo changed the locked rate and added points just days before closing after an underwriting error. So buyers should get the rate lock in writing and confirm the terms well before closing day.

Google and ConsumerAffairs

As of June 2026, Tomo holds about 4.4 stars on Google and about 4.7 stars on ConsumerAffairs. Both sites echo the same themes. Buyers love the rates and the savings. Some wish the communication ran smoother.

Tomo Mortgage pros and cons

Pros

- Posts real rates online, so buyers can compare before they apply

- Charges $0 in lender fees, which cuts the upfront cost

- Closes 98 percent of loans on time, by its own count

- Offers TrueRate, a free tool that shows fair rates across lenders

- Funds loans fast, with an average close of about 25 days

- Holds strong scores on Trustpilot, Zillow, Bankrate, and ConsumerAffairs

- Backed by major investors and has funded more than $3 billion in loans

Cons

- Focuses on purchases, so refinancing is open only to current customers

- Not available in every state

- No USDA loans and no home equity products

- Some buyers report slow replies during underwriting

- The rate lock lasts only 30 days, shorter than some rivals

- May sell the loan to another servicer after closing

- Younger company with a thinner review history than big banks

Who Tomo Mortgage is best for

Tomo Mortgage works best for home buyers who want low rates and no lender fees. It fits first-time and repeat buyers who feel fine working online. Buyers who have lost a deal to a slow closing will value its 98 percent on-time record. People who want to see a real rate before they commit will get the most from it.

Who should avoid Tomo Mortgage

Tomo is a poor fit for buyers in states where it is not licensed. It also falls short for anyone who needs a refinance, a home equity loan, or a USDA loan. Buyers who want in-person meetings and lots of hand-holding may prefer a local lender. People with complex income, like the self-employed, should confirm Tomo can handle their file before they apply.

Tomo Mortgage vs. Rocket Mortgage

Rocket Mortgage is the lender Tomo gets compared to most. Both work online. They differ in key ways. Here is how they line up.

- Fees. Tomo charges $0 in lender fees. Rocket’s origination fees often run about $1,200 or more.

- Rates. Tomo posts rates that often beat the market. Rocket rarely shows a personal rate without the buyer’s contact info.

- States. Rocket lends in all 50 states. Tomo lends in more than 40 states and Washington, D.C.

- Products. Rocket offers refinances, USDA loans, and home equity products. Tomo does not.

- Reviews. Rocket has tens of thousands of reviews. Tomo has fewer, but its scores are strong.

For buyers in Tomo’s states who want low cost and clear pricing, Tomo has the edge on price. For buyers who need a wider product range or live outside Tomo’s footprint, Rocket is the safer pick. Buyers weighing other online lenders can also compare Tomo with Newrez.

Is Tomo Mortgage legitimate?

Yes. Tomo Mortgage is a licensed, legitimate lender. Its NMLS ID is 2059741, and it operates as a licensed mortgage broker. Bankrate named it a Best Online Lender for 2026. It holds a 4.5 rating on Trustpilot and about 4.6 on Zillow from real buyers. We found no major regulatory action against it as of this review. The r/loanoriginators thread reflects industry surprise at its low pricing, not concern about fraud.

Tomo Mortgage review verdict

Tomo Mortgage is a strong and honest choice for home buyers. Its no-fee model and posted rates set it apart from both banks and big online lenders. It earns high marks on Trustpilot, Zillow, and Bankrate, and it closes loans fast. The main trade-off is service that can vary, with a few buyers reporting slow replies. For buyers in Tomo’s states who want a low rate and no lender fees, a quick Tomo quote is well worth the time.

Tomo Mortgage frequently asked questions

Is Tomo Mortgage legit?

Yes. Tomo is a licensed mortgage broker with NMLS ID 2059741. It has funded more than $3 billion in loans and earns strong reviews on Trustpilot, Zillow, and Bankrate.

What credit score do you need for Tomo Mortgage?

You need about 580 for a conventional or FHA loan. A score of 700 or higher helps you earn the lowest rates.

Does Tomo Mortgage really charge no fees?

Yes. Tomo charges no lender fees, such as origination or underwriting fees. You still pay third-party closing costs like title and appraisal.

What states does Tomo Mortgage serve?

Tomo lends in more than 40 states plus Washington, D.C. It is online only, with no branches.

Does Tomo Mortgage offer refinancing?

Tomo focuses on home purchases. It offers refinancing only to current customers and does not offer home equity products.

Disclaimer. This article is for informational purposes only. It is not legal, financial, or tax advice. Mortgage rates change daily. The rates noted here reflect data pulled in June 2026 and may differ today. Loan approval depends on credit, income, and property review. Compare several lenders before you choose. Tomo Mortgage is not available in all states.

Sponsored Advertising Content:

Advertorial or Sponsorship User published Content does not represent the views of the Company or any individual associated with the Company, and we do not control this Content. In no event shall you represent or suggest, directly or indirectly, the Company's endorsement of user published Content.

The company does not vouch for the accuracy or credibility of any user published Content on our Website and does not take any responsibility or assume any liability for any actions you may take as a result of reading user published Content on our Website.

Through your use of the Website and Services, you may be exposed to Content that you may find offensive, objectionable, harmful, inaccurate, or deceptive.

By using our Website, you assume all associated risks.This Website contains hyperlinks to other websites controlled by third parties. These links are provided solely as a convenience to you and do not imply endorsement by the Company of, or any affiliation with, or endorsement by, the owner of the linked website.

Company is not responsible for the contents or use of any linked website, or any consequence of making the link.

This content is provided by New Start Advantage LLC through a licensed media partnership with Inquirer.net. Inquirer.net does not endorse or verify partner content. All information is for educational purposes only and does not constitute financial advice. Offers and terms may change without notice.