Advertorial or Sponsorship User published Content does not represent the views of the Company or any individual associated with the Company, and we do not control this Content. In no event shall you represent or suggest, directly or indirectly, the Company's endorsement of user published Content.

The company does not vouch for the accuracy or credibility of any user published Content on our Website and does not take any responsibility or assume any liability for any actions you may take as a result of reading user published Content on our Website.

Through your use of the Website and Services, you may be exposed to Content that you may find offensive, objectionable, harmful, inaccurate, or deceptive.

By using our Website, you assume all associated risks.This Website contains hyperlinks to other websites controlled by third parties. These links are provided solely as a convenience to you and do not imply endorsement by the Company of, or any affiliation with, or endorsement by, the owner of the linked website.

Company is not responsible for the contents or use of any linked website, or any consequence of making the link.

Acima Leasing Reviews and Ratings

Acima Leasing official logo

Acima is one of the most widely available lease-to-own platforms in the United States. The company works with more than 15,000 retail partners. It helps consumers take home furniture, electronics, appliances, tires and other merchandise without perfect credit. For anyone researching an Acima review, the most important thing to understand is the total cost.

Acima’s own disclosures state that standard agreements “may cost more than double the cash price.” For a $600 item, that means the consumer could pay $1,200 or more through the full 12-month lease. That is a significant premium over the retail price.

This review covers everything a potential customer needs to know. It breaks down how Acima works, what it actually costs and what real customers are saying. It also examines whether this platform makes sense for different types of consumers.

Evaluate these top-rated lenders to find a better match for your credit tier:

- Direct Lending Excellence: Matches you with the best loans.

- Loans ranging from $2,500 to $100,000

- Flexible terms: 3 to 120 months, 24 hours post-approval

- Same day approval

- Direct Lending Excellence: Matches you with the best loans with optimal loan terms.

- Comprehensive Loan Network: Loans ranging from $2,500 to $50,000

- Flexibility & Speed: Flexible terms from 3 to 120 months, 24 hours post-approval.

- Loan amounts up to $100,000

- Custom Terms: Repayment periods from 12 to 60 months with fast 48-hour approvals.

- Trusted Expertise: Recognized for ethical lending and innovative financial solutions.

What is Acima?

Acima Leasing homepage

Acima Digital, LLC operates as a lease-to-own service under Upbound Group, Inc. (traded on NASDAQ under UPBD). The company was previously known as Acima Credit and Simple Finance Technology Corp before rebranding. Upbound Group, formerly Rent-A-Center, acquired Acima in 2021.

The company is headquartered in Draper, Utah and has been in business for more than 13 years according to its BBB profile. Acima partners with over 15,000 retailers nationwide. This gives consumers access to everyday essentials and big-ticket items alike.

Acima offers two main products. The first is its core lease-to-own service. The second is the Acima Classic Credit Mastercard. This is a separate credit card issued by The Bank of Missouri and serviced by Concora Credit Inc. Neither The Bank of Missouri nor Concora Credit is affiliated with Acima Digital or its affiliates.

The platform is not available in Minnesota, New Jersey or Wisconsin. All other U.S. states are eligible. Specific promotions may carry additional restrictions.

How Acima leasing works

Acima’s lease-to-own process follows five main steps.

Step 1. Application

The consumer applies through the Acima app, the Acima website or at a participating retailer. Acima obtains information from consumer reporting agencies during the application. Perfect credit is not required, but not all applicants are approved.

Step 2. Approval and lease amount

Once approved, the consumer receives a lease amount. This represents the cash price Acima will pay to the retailer on the consumer’s behalf. The maximum approval amount is $5,000. Higher amounts may require an in-store application.

Step 3. Shopping

The consumer shops at any participating retailer up to the approved amount. The Acima Marketplace app also provides access to Amazon, Best Buy and Walmart.

Step 4. Checkout and lease signing

At checkout, the consumer signs the lease agreement and makes an initial payment. Some locations offer a “Start a Lease for $10” promotion. This defers the first renewal payment but does not reduce the total cost.

Step 5. Ownership or return

The consumer can reach ownership through three paths. They can pay through the full 12-month standard agreement. They can exercise the early purchase option to reduce total cost. Or they can return the item and cancel the lease at any time without penalty. The item must be in good condition upon return.

The early purchase option is the most important tool for reducing total cost. Consumers who pay within 90 days pay the Acima Cash Price plus a purchase fee of typically $25. Those who pay after 90 days but before the lease ends pay a lump sum of roughly 65 percent of the remaining balance.

Acima pricing and fees

This is the most critical section for any potential Acima customer. The company’s own disclosure is direct. “Standard agreement offers 12 months to ownership if you choose to make each lease renewal payment, which may cost more than double the cash price.”

Here is what that looks like in real dollars for a $600 item.

- Buying at retail price costs $600

- Using the 90-day early purchase option costs the retail price plus a fee of roughly $25, totaling approximately $625

- Paying after 90 days but before the lease ends costs a reduced lump sum, typically 65 percent of the remaining balance plus what has already been paid

- Completing the full 12-month lease may cost $1,200 or more, which is more than double the original retail price

The “Start a Lease for $10” promotion deserves special attention. The fine print states this offer “will not reduce the number of payments, total amount necessary to acquire ownership, or purchase option amount.” The $10 is an entry cost that defers the first renewal payment. It is not a discount on the total lease. Customers in California pay a $0 initial rent payment and a $10 processing fee to start.

Acima is not a loan. It is a lease. Because of this classification, the Truth in Lending Act (TILA) does not require Acima to disclose an annual percentage rate (APR). All costs in this review are presented in dollar terms only.

Acima Classic Credit Mastercard

Acima has introduced a credit card product that is separate from its core lease-to-own service.

The Acima Classic Credit Mastercard is issued by The Bank of Missouri and serviced by Concora Credit Inc. It is an unsecured credit card that can be used anywhere Mastercard is accepted in the United States. No security deposit is required.

Here are the key terms of the card.

- The purchase APR is 35.9 percent

- The cash advance APR is 35.9 percent

- No security deposit is required

- Applicants must be at least 18 years old with a valid Social Security number and a physical U.S. address

- Approval involves a review of income, debt and identity verification

- If approved, a new account and a hard credit inquiry will appear on the consumer’s credit report

- If not approved, no hard inquiry will appear

This card is a completely separate product from the Acima lease. A consumer can hold both the lease and the Mastercard at the same time. However, disputes related to the card go to The Bank of Missouri and Concora Credit. They do not go to Acima Digital.

The 35.9 percent APR is high compared to most traditional credit cards. Consumers should weigh this rate carefully before applying.

What you can lease through Acima

Acima’s retail partner network spans more than 15,000 locations. These include both in-store and online retailers. Available merchandise categories include furniture, electronics, appliances, tires, mattresses, mobile phones and other household items.

The Acima Marketplace app provides access to major retailers including Amazon, Best Buy and Walmart. However, not all products at every partner retailer are eligible for leasing. The maximum lease amount is $5,000. In-store applications may be required for higher approval amounts.

Each approval lasts for 90 days and applies only to the store where the consumer originally applied. Shopping at a different retailer requires a new application. This cancels the original approval. Consumers can only have one active approval at a time.

Acima eligibility requirements

Acima does not require perfect credit. The company states it “regularly approves customers with less than perfect credit history.” However, not all applicants are approved.

General eligibility factors include the following.

- Minimum age of 18 years

- An active bank account or debit card

- Proof of income

- Identity verification

- Acima obtains information from consumer reporting agencies during the application

The Acima Classic Credit Mastercard has a separate application process. It includes its own eligibility requirements such as a review of income and debt levels.

Acima is not available in Minnesota, New Jersey or Wisconsin. Additional state restrictions may apply to specific promotions or the Mastercard product.

What customers say about Acima

Trustpilot reviews

Acima Trustpilot profile

Acima has more than 23,000 reviews on Trustpilot. Customer feedback is mixed. Many reviewers praise the quick approval process and the ease of making payments. Others express frustration over hidden fees, high total costs and billing disputes.

Positive reviews frequently mention the simple application process and helpful customer service. Negative reviews tend to focus on the final cost of ownership being much higher than expected. Payment processing errors and difficulty reaching support are also common themes.

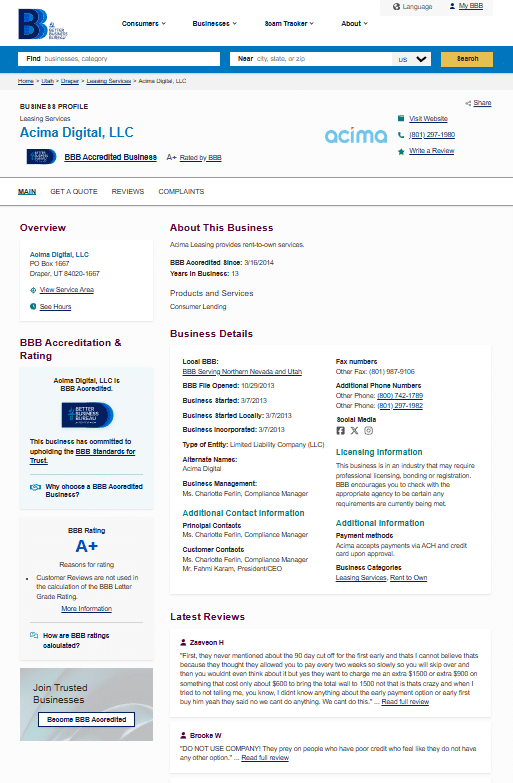

Better Business Bureau (BBB) reviews

Acima Digital BBB business profile

Acima Digital, LLC holds an A+ rating with the BBB and has been accredited since 2014. However, the customer review rating tells a different story. The company holds a 1.06-star rating out of five based on customer reviews.

Acima has received nearly 600 complaints with the BBB in the past year alone. The majority of complaints involve billing issues, payment processing errors and service disputes. Common themes include unexpected total costs, difficulty with the return and cancellation process and third-party debt collection practices.

The A+ rating reflects the company’s responsiveness to complaints rather than overall customer satisfaction.

Reddit reviews

Organic discussions about Acima appear frequently on Reddit. This is particularly true in r/personalfinance, r/povertyfinance and r/smallbusiness.

One highly upvoted post on r/personalfinance titled “Do not use Acima Leasing” describes a consumer who leased a $2,500 MacBook Pro. The total lease amount was listed at $6,400 if not paid within the 12-month term. The post warns readers about the gap between what sales representatives say and what the contract actually states.

On r/smallbusiness, a retailer calculated that customers end up paying “almost double the financed amount” over a 12-month term. The same post notes that the 90-day payoff option requires the customer to call or chat with Acima to set it up.

Other recurring Reddit themes include payment processing failures, the difficulty of exercising the early purchase option and confusion around the “Start a Lease for $10” promotion.

App Store and Google Play

The Acima app holds a 4.8 out of five rating on the Apple App Store based on more than 24,000 ratings. Positive reviews highlight the easy application process and in-app lease management.

On Google Play, the app holds a 3.0 out of five rating. Common complaints in low-rated reviews mention payment processing errors, NSF (insufficient funds) fee disputes and difficulty reaching customer service.

Acima complaints and red flags

Several notable issues deserve attention before signing an Acima lease.

Consumer Financial Protection Bureau (CFPB) lawsuit and dismissal. In July 2024, the CFPB filed a lawsuit against Acima Holdings, LLC, Acima Digital, LLC and Acima’s founder Aaron Allred. The CFPB alleged that Acima used deceptive dark patterns to obscure the true cost of its agreements. The Bureau also alleged violations of the Consumer Financial Protection Act, the Fair Credit Reporting Act, TILA and the Electronic Fund Transfer Act. However, in March 2025 the CFPB voluntarily dismissed the case with prejudice.

Total cost surprise. The single most common complaint across Trustpilot, BBB and Reddit is that the total cost of ownership far exceeds expectations. Consumers who do not exercise the early purchase option may pay more than double the retail price.

“Start a Lease for $10” confusion. This promotion does not lower the total cost. The fine print confirms it “will not reduce the number of payments, total amount necessary to acquire ownership, or purchase option amount.” Consumers who interpret this as a discount are misunderstanding the offer.

Third-party debt collection. Some BBB complaints describe aggressive collection calls from third parties after Acima sold delinquent accounts. One complaint detailed threatening voicemails to family members about “defrauding a financial institution.”

Payment processing issues. Multiple sources report automatic payment failures followed by NSF fees, even when funds are available in the consumer’s account.

Acima outcomes and success rates

Acima does not publicly disclose specific approval rates or success benchmarks. The company states that it “regularly approves customers with less than perfect credit history.” Approval amounts range from $300 to $5,000 based on the consumer’s financial profile.

The most meaningful outcome for consumers depends on which payment path they choose. Those who exercise the 90-day early purchase option pay close to the retail price plus a small fee. Those who complete the full 12-month lease may pay more than double the retail price.

Consumers who return the item and cancel the lease are responsible for all payments made up to the return date. Payments already made before the return are not refunded.

According to one Reddit retailer, the company claims that “the majority of customers use the 90-Day option” and that “90 percent of the applicants are approved.” These figures have not been independently verified.

Acima pros and cons

Pros

- More than 15,000 retail partners including app-based access to Amazon, Best Buy and Walmart

- The early purchase option significantly reduces total cost for consumers who can pay within 90 days

- Consumers can return the item and cancel the lease at any time without penalty

- The Acima Classic Credit Mastercard uses a soft-check-first application, with a hard inquiry appearing only upon approval

- Quick approval process with flexible payment schedules aligned to paydays

- The Acima app holds a 4.8 rating on the Apple App Store with strong user reviews

Cons

- The full 12-month lease may cost more than double the retail price per Acima’s own disclosure

- The “Start a Lease for $10” promotion does not reduce the total cost of ownership

- The Acima Classic Credit Mastercard carries a 35.9 percent APR and is issued by a third-party institution

- Not available in Minnesota, New Jersey or Wisconsin

- Nearly 600 BBB complaints in the past year, primarily about billing and payment processing

- The CFPB filed a lawsuit in 2024 alleging deceptive practices, though it was voluntarily dismissed in 2025

- “No credit needed” does not mean guaranteed approval

Who should use Acima

Acima may be a practical option for a narrow group of consumers. The ideal candidate meets all of the following conditions.

- They need a specific item immediately and cannot wait

- They do not qualify for a store credit card, a zero percent APR financing offer or a buy-now-pay-later (BNPL) installment plan

- They have reviewed and accepted the total cost structure

- They have a concrete plan to exercise the early purchase option as early as possible

- They live in a state where Acima is available

The Acima Marketplace app adds value for consumers who want access to major online retailers within the lease-to-own framework. The Acima Classic Credit Mastercard is worth evaluating for consumers who want to build credit alongside their lease, with the understanding that it carries a 35.9 percent APR.

Who should look elsewhere instead of Acima

Acima is not the right choice for everyone. The following consumers should explore other options.

- Anyone who can qualify for a store credit card with a zero percent promotional period

- Anyone with access to a BNPL product that offers fixed payments and a lower total cost

- Residents of Minnesota, New Jersey or Wisconsin

- Anyone who interprets the “Start a Lease for $10” promotion as a cost reduction

- Anyone who plans to complete the full 12-month lease without using the early purchase option

Better alternatives include zero percent APR store financing, credit union personal loans and BNPL installment options through providers like Affirm or Klarna. These alternatives typically carry lower total costs and more transparent pricing.

Acima vs Snap Finance

Snap Finance is one of the most common alternatives to Acima in the lease-to-own space. Here is how the two compare.

- Approval amounts. Both Acima and Snap Finance offer approval amounts ranging from $300 to $5,000

- Early purchase option. Acima offers a 90-day early purchase option. Snap Finance offers a 100-day early buyout option, giving consumers 10 additional days to pay the reduced price

- Payment flexibility. Both platforms offer flexible payment schedules aligned to paydays, including weekly, biweekly and monthly options

- Credit requirements. Both Acima and Snap Finance market themselves as no-credit-needed options. Neither requires perfect credit for approval

- Retailer network. Acima claims more than 15,000 retail partners. Snap Finance also partners with thousands of retailers across the United States

- App experience. The Acima app holds a 4.8 rating on the Apple App Store and 3.0 on Google Play. Snap Finance also offers a mobile app for managing payments and shopping

The biggest difference is the early purchase window. Snap Finance gives consumers 10 extra days to pay the cash price plus a small fee. For consumers who plan to pay off their lease quickly, that additional window could save hundreds of dollars.

Bottom line on Acima

Acima is conditionally recommended for a specific type of consumer. It is a workable option for credit-constrained shoppers who need immediate access to merchandise, have no lower-cost financing alternative and commit to using the early purchase option as soon as possible.

The total cost structure is the defining factor. Consumers who pay within 90 days will spend close to the retail price. Consumers who complete the full 12-month lease will pay more than double. That gap is too large to ignore.

The early purchase option is the single most important lever available to reduce cost. Consumers who cannot realistically exercise it should strongly consider other options before signing a lease.

Before signing any agreement, review the full lease terms and confirm the total cost of ownership in writing. Compare rates from store credit cards, credit unions and BNPL providers. Acima should be a last resort, not a first choice.

Disclaimer. This article is for informational purposes only and does not constitute legal, financial or tax advice. Always consult a licensed professional for advice tailored to your situation.

Frequently asked questions about Acima

Is Acima a legitimate company?

Yes. Acima Digital, LLC has been in business for over 13 years and holds an A+ rating with the BBB. The company partners with more than 15,000 retailers across the United States. However, the total cost of leasing through Acima can significantly exceed the retail price. Consumers should review all terms carefully before signing any agreement.

Does Acima check your credit?

Acima obtains information from consumer reporting agencies during the application process. The company markets itself as a “no credit needed” option, meaning perfect credit is not required. However, not all applicants are approved. The specific type of credit inquiry for the lease application should be confirmed before applying. The Mastercard product conducts a hard inquiry only upon approval.

How much does Acima actually cost?

According to Acima’s own disclosure, the standard 12-month agreement “may cost more than double the cash price.” For a $600 item, the total cost could exceed $1,200 if the consumer completes all scheduled payments. The early purchase option within 90 days reduces the total to approximately the retail price plus a $25 fee.

Can you return items leased through Acima?

Yes. Consumers can return leased items at any time without penalty as long as the item is in good condition. However, payments already made before the return are not refunded. The consumer is responsible for all payments made during the time they had the item.

What states is Acima not available in?

Acima is not available in Minnesota, New Jersey or Wisconsin. Specific promotions or the Acima Classic Credit Mastercard may carry additional state-level restrictions. Consumers should verify availability in their state before applying.

Sponsored Advertising Content:

Advertorial or Sponsorship User published Content does not represent the views of the Company or any individual associated with the Company, and we do not control this Content. In no event shall you represent or suggest, directly or indirectly, the Company's endorsement of user published Content.

The company does not vouch for the accuracy or credibility of any user published Content on our Website and does not take any responsibility or assume any liability for any actions you may take as a result of reading user published Content on our Website.

Through your use of the Website and Services, you may be exposed to Content that you may find offensive, objectionable, harmful, inaccurate, or deceptive.

By using our Website, you assume all associated risks.This Website contains hyperlinks to other websites controlled by third parties. These links are provided solely as a convenience to you and do not imply endorsement by the Company of, or any affiliation with, or endorsement by, the owner of the linked website.

Company is not responsible for the contents or use of any linked website, or any consequence of making the link.

This content is provided by New Start Advantage LLC through a licensed media partnership with Inquirer.net. Inquirer.net does not endorse or verify partner content. All information is for educational purposes only and does not constitute financial advice. Offers and terms may change without notice.