Advertorial or Sponsorship User published Content does not represent the views of the Company or any individual associated with the Company, and we do not control this Content. In no event shall you represent or suggest, directly or indirectly, the Company's endorsement of user published Content.

The company does not vouch for the accuracy or credibility of any user published Content on our Website and does not take any responsibility or assume any liability for any actions you may take as a result of reading user published Content on our Website.

Through your use of the Website and Services, you may be exposed to Content that you may find offensive, objectionable, harmful, inaccurate, or deceptive.

By using our Website, you assume all associated risks.This Website contains hyperlinks to other websites controlled by third parties. These links are provided solely as a convenience to you and do not imply endorsement by the Company of, or any affiliation with, or endorsement by, the owner of the linked website.

Company is not responsible for the contents or use of any linked website, or any consequence of making the link.

TitleMax Reviews and Ratings

TitleMax official company logo

TitleMax is one of the largest title loan and pawn companies in the United States. The company runs more than 850 locations across 16 states and lends up to $10,000 using a car title as collateral. Borrowers can get cash in as little as 30 minutes.

But is TitleMax a safe choice for emergency cash? The answer is not straightforward, as TitleMax has faced two enforcement actions from the Consumer Financial Protection Bureau (CFPB). The first came in 2016 with a $9 million penalty. The second followed in 2023 with a $10 million fine and more than $5 million in consumer relief. Both cases involved deceptive lending practices and violations of the Military Lending Act.

This TitleMax review covers the company’s products, rates, eligibility requirements and customer feedback. It also examines regulatory history and compares TitleMax to LoanMart. Readers will walk away with a clear picture of the risks and benefits before applying.

Evaluate these top-rated lenders to find a better match for your credit tier:

- Direct Lending Excellence: Matches you with the best loans.

- Loans ranging from $2,500 to $100,000

- Flexible terms: 3 to 120 months, 24 hours post-approval

- Same day approval

- Direct Lending Excellence: Matches you with the best loans with optimal loan terms.

- Comprehensive Loan Network: Loans ranging from $2,500 to $50,000

- Flexibility & Speed: Flexible terms from 3 to 120 months, 24 hours post-approval.

- Loan amounts up to $100,000

- Custom Terms: Repayment periods from 12 to 60 months with fast 48-hour approvals.

- Trusted Expertise: Recognized for ethical lending and innovative financial solutions.

What is TitleMax?

. The company describes itself as one of the nation's largest title lending companies, with over 900 locations spanning 14 states and more than 2,000 team members nationwide.](https://usa.inquirer.net/files/2026/05/titlemax-about-us-page.png)

TitleMax About Us webpage

The company offers car title loans, car title pawns (in Georgia), motorcycle title loans, motorcycle title pawns and personal loans. TitleMax accepts all credit types and focuses on borrowers who may not qualify for traditional bank loans.

TitleMax works differently in Texas, where it is registered as a Credit Service Organization (CSO) and licensed as a Credit Access Business (CAB). This means TitleMax does not lend directly in Texas but instead arranges loans through a separate lender. Borrowers in Texas should know that their contract is with that other company, not TitleMax.

In Georgia, TitleMax operates under state pawn laws instead of standard lending laws. This matters because pawn transactions carry different rules for consumer protections, repayment options and defaults.

How TitleMax loans and pawns work

In-store process

Borrowers visit a TitleMax store with a clear car title, the vehicle, a photo ID and proof of income. A store associate appraises the car on site. If approved, the borrower receives a loan offer based on the car’s value and ability to repay. Cash can be available in as little as 30 minutes, and the borrower keeps driving the car during repayment. TitleMax returns the title once the loan is paid off.

Online appraisal option

TitleMax also offers an online option through its Fast Track Appraiser app. The app lets borrowers check their car’s value remotely using a phone camera. However, the app requires video, audio, location and camera access, and the initial estimate may change after further review. Borrowers who prefer not to share this level of device access will need to visit a store instead.

Title pawn distinction in Georgia

As noted above, Georgia transactions follow pawn laws rather than lending laws. This changes how defaults, redemptions and repayment are handled. Borrowers in Georgia should confirm they understand the pawn agreement terms before signing.

Texas CSO model

As mentioned earlier, TitleMax arranges loans through a third-party lender in Texas. Because of this, borrowers should confirm who their contract is with and where to direct any disputes.

Repossession risk

Failing to repay a title loan can result in losing the vehicle, as TitleMax holds the title as collateral. If the borrower defaults, the company can repossess and sell the car. The borrower may still owe a remaining balance after the sale, depending on state law.

TitleMax loan products

Car title loans and pawns

This is the core TitleMax product, offering borrowers up to $10,000 secured by a car title. Loan amounts vary by state. In Mississippi, the maximum is $3,250. In Tennessee, the combined maximum is $6,500, which breaks down into a title pledge (up to $2,500) and a secured credit line (up to $4,000).

TitleMax also offers a competitor payoff program. The company says it will pay off a title loan from a rival lender and lower the rate. However, borrowers should verify whether that rate reduction is guaranteed before signing.

Certain borrowers may qualify for up to $25,000 in select markets. This is uncommon and not the standard product.

Motorcycle title loans and pawns

TitleMax offers motorcycle title loans and pawns at participating locations. In Arizona, the maximum is $2,500 for motorcycle collateral. In Tennessee, the pledge maximum for motorcycles is also $2,500, while the cap in other markets is $3,000. Availability varies by location.

Personal loans

TitleMax also offers unsecured personal loans at select store locations that do not require a car title. The in-store process takes about 30 minutes, while online requests are processed by the next business day. In South Carolina, the minimum loan amount is $601 in-store and $610 online. Not all stores carry this product.

TitleMax rates and fees

TitleMax does not publish rates or fee schedules on its website, making it difficult for borrowers to compare costs before visiting a store.

Title loan fees vary by state due to different regulatory rules, so borrowers need to research their own state’s fee structure. Here is what publicly available data shows about costs in key TitleMax markets.

- In Georgia, title pawns follow pawnbroker fee rules. State law allows pawn shops to charge fees that can translate to APRs exceeding 200 percent when annualized

- The CFPB noted in its 2016 enforcement action that some TitleMax title loans carried APRs of up to 300 percent

- Nevada’s consumer notice on the TitleMax website warns that title loans should be used for short-term needs only. Borrowers with credit difficulties should seek counseling first

- In New Mexico, TitleMax publishes a fee schedule for installment loans. APRs on these products depend on the loan amount and repayment term

Borrowers should request the full fee schedule in writing before signing any agreement. Title loan fees, when annualized, commonly exceed 100 percent APR.

TitleMax eligibility requirements

TitleMax requires the following to apply for a title loan.

- A clear car title registered in the borrower’s name

- The vehicle must be present for appraisal (in-store) or accessible through the Fast Track app (online)

- A valid government-issued photo ID such as a driver’s license

- Proof of income or ability to repay

- Compliance with any state database eligibility rules

In addition, borrowers should be aware of the following restrictions.

- Active-duty military members, spouses and dependents cannot apply under the Military Lending Act (MLA)

- In Alabama, the minimum age for a secured product is 19

- TitleMax advertises “all credit welcome” for title products, but the fine print notes that some products require a credit check

- Online applications may not be available in all states

Therefore, borrowers should verify their state’s availability through the TitleMax store locator before applying. TitleMax has exited certain states following regulatory pressure.

What customers say about TitleMax

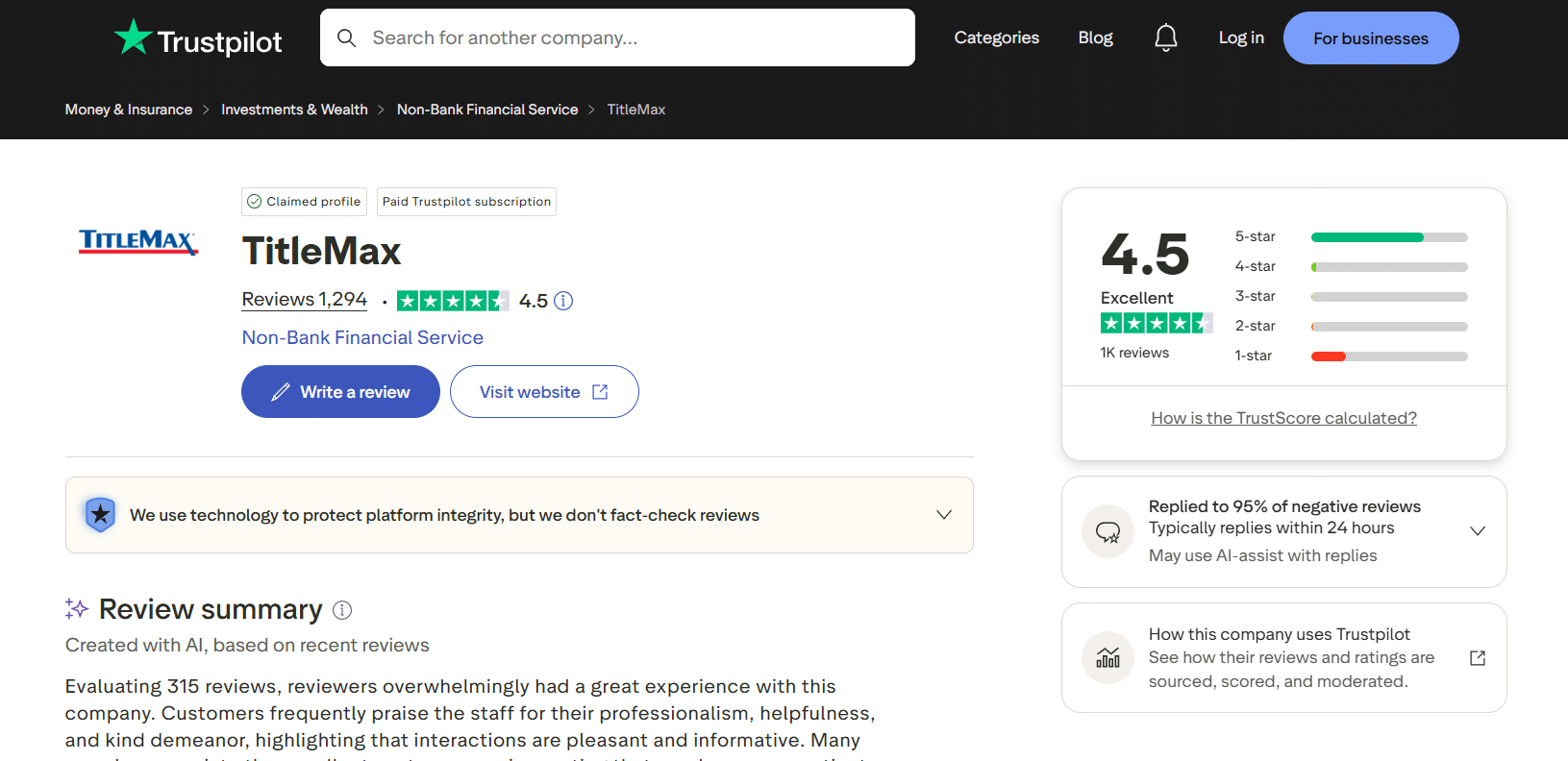

Trustpilot reviews

TitleMax Trustpilot profile

TitleMax holds a 4.5-star rating on Trustpilot based on more than 1,290 reviews. Many positive reviews highlight fast approval times, friendly staff and a smooth experience. Customers frequently praise individual employees by name and call the process quick.

However, negative reviews paint a different picture. Some borrowers report confusion about the 30-day loan structure, while others express frustration with high renewal fees that do not reduce the principal balance. TitleMax does respond to reviews on the platform.

Better Business Bureau (BBB) reviews

TitleMax holds an A+ rating with the BBB but is not an accredited business. This means TitleMax has not agreed to BBB Standards for Trust. The company has a notable volume of complaints on file.

Common complaint themes include the following.

- Hidden fees and charges that were not clearly explained at signing

- Difficulty paying down the principal balance due to high renewal costs

- Aggressive collection practices and repossession threats

- Confusion about payment structures and loan terms

One notable BBB complaint came from a veteran who paid $1,000 to $1,750 per month for 23 months on a $10,000 loan and still owed the original balance. This pattern mirrors the issues documented in the 2016 CFPB enforcement action.

Reddit reviews

TitleMax appears frequently across personal finance subreddits, with threads in r/personalfinance, r/povertyfinance, r/titleloan and r/legaladvice revealing common patterns.

- Borrowers report paying far more than the original loan amount over time without reducing the balance

- Several users describe the repossession process as sudden and stressful

- Texas borrowers express frustration with the CSO model and unclear contract terms

- Many users recommend title loans only as an absolute last resort

One r/personalfinance post described paying half of each paycheck for a full year on a $5,000 loan with no clear path to payoff. The user was considering surrendering the vehicle.

Reddit sentiment tends to lean negative, but the volume and consistency of these accounts suggest real patterns that potential borrowers should consider.

ConsumerAffairs reviews

TitleMax is listed as a ConsumerAffairs Authorized Partner, meaning the company pays for placement on the platform. This is a commercial relationship, not an editorial endorsement. Borrowers should keep this context in mind when reading reviews.

Reviews on the platform are mixed. Positive reviews praise fast service and helpful staff. Negative reviews cite high interest rates, surprise renewal fees and long-term cost concerns.

Google reviews

TitleMax operates a large network of physical stores, making Google Reviews one of the richest sources of ground-level customer feedback. Reviews across store locations in Georgia, Tennessee, Nevada and South Carolina show consistent trends.

Positive Google reviews frequently mention helpful staff, fast service and a straightforward process. Many borrowers appreciate the ability to get cash quickly during emergencies.

Negative reviews, on the other hand, focus on high costs that were not fully understood at signing. Some reviewers describe feeling stuck in renewal cycles, while others report difficulty reaching customer service. Ratings vary significantly by store, so borrowers should check reviews for their nearest location before visiting.

TitleMax complaints and red flags

This section covers the most significant risk factors tied to TitleMax.

2016 CFPB consent order

In September 2016, the CFPB took action against TMX Finance LLC for unfair lending and debt collection practices in Alabama, Georgia and Tennessee.

The CFPB found that store employees offered borrowers a “monthly option” and a “Voluntary Payback Guide” that obscured the true cost of renewing the loan multiple times. The company also conducted in-person “field visits” to homes and workplaces to collect payments, exposing private debt information to employers, friends and family.

TMX Finance agreed to stop using the payback guide, end field visits, submit to compliance monitoring and pay a $9 million civil penalty.

2023 CFPB consent order

In February 2023, the CFPB filed a second enforcement action against TMX Finance LLC. This one focused on Military Lending Act (MLA) violations. The CFPB found that from October 2016 to September 2021, TitleMax made 2,670 loans to protected borrowers in violation of MLA rules. Protected borrowers include active-duty military members, spouses and dependents.

The company also added restrictive legal notice terms to loan contracts that made it very difficult for borrowers to dispute charges. The CFPB ordered a $10 million fine and more than $5 million in consumer relief.

This $15 million penalty marked the CFPB’s first enforcement against a nonbank lender for providing title loans to military families.

State regulatory actions

TitleMax has also faced scrutiny from state regulators. In Georgia, investigative reporting highlighted how pawn laws create a loophole that allows title lenders to charge APRs of 200 to 300 percent. TitleMax has exited or scaled back in certain states following regulatory pressure. Borrowers should verify current state availability through the store locator.

Add-on product concerns

The 2016 CFPB case also flagged how loan terms were presented to borrowers. Borrowers should ask whether any extras like roadside assistance or insurance are included in their loan agreement. They should also verify whether these products are optional or built into the total cost.

TitleMax outcomes and success rate

TitleMax does not publish approval rates or performance data on its website, which limits the ability to evaluate outcomes objectively.

Still, publicly available data reveals the following patterns.

- The CFPB’s 2016 case showed that many borrowers renewed loans repeatedly, paying far more than the original amount over time

- BBB and Reddit posts consistently describe borrowers paying multiples of their loan amount before reaching payoff

- Title loans are typically due in 30 days, and many borrowers renew multiple times, which raises the total cost substantially

- Paying off a title loan depends on the borrower’s ability to cover the full balance within the initial term or a few renewal cycles

For this reason, borrowers should have a concrete repayment plan before signing. Without one, the risk of paying far more than the borrowed amount increases significantly.

TitleMax pros and cons

Pros

- More than 850 stores across 16 states provide strong physical access for borrowers in active markets

- All credit types are accepted with no stated minimum credit score requirement

- Multiple product types under one brand, including title loans, pawns, motorcycle loans and personal loans

- Competitor payoff program allows borrowers to refinance a title loan from another company

- Online appraisal through the Fast Track Appraiser app reduces the need for an initial store visit

- Customer portal and text reminder system help borrowers manage payments

Cons

- Two CFPB enforcement actions resulted in $19 million in combined penalties for deceptive practices and MLA violations

- Rates and fees are not published online, preventing borrowers from comparing costs before visiting

- In Texas, TitleMax is not the direct lender, which reduces transparency about the actual loan provider

- Some states have been exited following regulatory pressure

- The Fast Track app requires location sharing, camera access and microphone access

- Mississippi caps loans at $3,250 and Tennessee caps at $6,500, limiting borrowing amounts

- Active-duty military members, spouses and dependents cannot use this product

- Multiple BBB and Reddit accounts describe repayment cycles where the principal balance barely decreases

TitleMax vs LoanMart

TitleMax and LoanMart are both major title loan companies in the United States. Here is how they compare across key factors.

- Application process. TitleMax is primarily branch-based with an online appraisal option. LoanMart focuses more on online lending and servicing

- Where they operate. TitleMax has 850+ physical stores in 16 states. LoanMart covers more states through online and partner channels

- Loan amounts. TitleMax offers up to $10,000 in most markets (up to $25,000 in select ones). LoanMart amounts vary by state and lending partner

- Rate transparency. Neither company publishes APR ranges on its website, which is a shared limitation for borrowers

- Funding speed. Both companies offer same-day funding for in-store applications

- Regulatory history. TitleMax has two CFPB enforcement actions totaling $19 million in penalties. Borrowers should research LoanMart’s record independently for comparison

- Texas lending model. TitleMax brokers loans through a third party in Texas. LoanMart’s servicing model may differ by state

- Customer reviews. TitleMax holds a 4.5-star Trustpilot rating from 1,290+ reviews. Both companies receive mixed feedback across platforms

Neither company is a clear winner across all categories. Borrowers should compare offers from both and read all terms carefully before signing.

Who should use TitleMax

TitleMax may work for a very specific type of borrower who meets all of the following conditions.

- Owns a car with a clear title and has no cheaper alternative for emergency cash

- Faces a genuine short-term financial need with a clear plan to repay the loan on time

- Lives near an active TitleMax location

- Has reviewed the state-specific fee schedule in writing before signing

- Is not an active-duty military member, spouse or dependent

The CFPB enforcement history does not automatically rule out TitleMax, but it is something every borrower should weigh carefully. Those who are concerned about collection practices or add-on product pressure should ask about these directly before signing any agreement.

This is not a long-term financial solution.

Who should avoid TitleMax

TitleMax is not the right fit for everyone. Borrowers should explore other options if any of the following apply.

- Active-duty military members, spouses and dependents are legally excluded under the MLA

- Borrowers in states where TitleMax no longer operates

- Anyone without a clear car title

- Borrowers who need more than $10,000 (the standard cap in most markets)

- Mississippi residents who need more than $3,250 or Tennessee residents who need more than $6,500

- Anyone with access to lower-cost alternatives such as credit union loans, personal installment loans or payment plans with creditors

- Borrowers who want to compare rate and fee details before visiting a store or submitting an application

For an online title loan option, LoanMart may offer a more accessible alternative. For lower-cost borrowing, credit union emergency loans typically carry much lower APRs.

TitleMax bottom line

TitleMax receives a conditional recommendation for a narrow group of borrowers. It serves as a fast cash option for someone with a clear car title, a genuine short-term need, no lower-cost alternative and a firm plan to repay within the initial loan term.

However, TitleMax carries a heavier regulatory burden than most competitors. Two CFPB enforcement actions totaling $19 million in penalties make it the most flagged brand in this review series. The 2016 action targeted deceptive lending practices, while the 2023 action addressed illegal loans to military families. These are critical facts that borrowers must weigh against the convenience and speed that TitleMax offers.

Rates are not published online, so borrowers must obtain the full fee schedule in writing before signing. Title loan costs, when annualized, can exceed 200 to 300 percent APR depending on the state.

For borrowers who want a cleaner regulatory record, LoanMart and LoanMax are worth comparing. Both have been reviewed in this series.

Disclaimer. This article is for informational purposes only and does not constitute legal, financial, or tax advice. Always consult a licensed professional for advice tailored to your situation.

Frequently asked questions about TitleMax

Is TitleMax safe to use?

TitleMax is a licensed lender operating across 16 states, but it has faced two CFPB enforcement actions for deceptive practices and MLA violations. Borrowers should read all terms carefully and request full fee disclosures before signing.

How fast is the TitleMax approval process?

TitleMax advertises in-store approval in as little as 30 minutes. Online applications through the Fast Track app may require a follow-up store visit for final paperwork in some states.

Does TitleMax affect your credit score?

TitleMax says all credit types are welcome for title products, but some products may involve a credit check. Defaulting on a title loan and having the balance sent to collections could negatively impact credit.

Can TitleMax repossess your car?

Yes. TitleMax holds the car title as collateral during the loan period. If the borrower defaults, TitleMax can repossess and sell the vehicle. The borrower may still owe a remaining balance after the sale.

What states does TitleMax operate in?

TitleMax currently operates in 16 states, including Alabama, Arizona, Georgia, Kansas, Mississippi, Nevada, New Mexico, South Carolina, Tennessee, Texas, Utah and Wisconsin. Availability changes over time, so borrowers should check the store locator for current locations.

Sponsored Advertising Content:

Advertorial or Sponsorship User published Content does not represent the views of the Company or any individual associated with the Company, and we do not control this Content. In no event shall you represent or suggest, directly or indirectly, the Company's endorsement of user published Content.

The company does not vouch for the accuracy or credibility of any user published Content on our Website and does not take any responsibility or assume any liability for any actions you may take as a result of reading user published Content on our Website.

Through your use of the Website and Services, you may be exposed to Content that you may find offensive, objectionable, harmful, inaccurate, or deceptive.

By using our Website, you assume all associated risks.This Website contains hyperlinks to other websites controlled by third parties. These links are provided solely as a convenience to you and do not imply endorsement by the Company of, or any affiliation with, or endorsement by, the owner of the linked website.

Company is not responsible for the contents or use of any linked website, or any consequence of making the link.

This content is provided by New Start Advantage LLC through a licensed media partnership with Inquirer.net. Inquirer.net does not endorse or verify partner content. All information is for educational purposes only and does not constitute financial advice. Offers and terms may change without notice.